Over the past two weeks, Bitcoin price appears to have lost momentum and some analysts are suggesting that bears will be in control for the foreseeable future.

Taking a look at derivatives market data provides a clearer picture of what is happening on the institutional side and how the moves of larger players may impact the spot markets.

After peaking at $10.6 billion on Jan. 14, the open interest on Bitcoin (BTC) scaled back to $8.4 billion. The Jan. 29 monthly expiry continues to stand apart, totaling 47% of the options in play.

Although a $4 billion expiry could be significant, one must consider that these options are split among calls (neutral-to-bullish) and the more bearish put options. Furthermore, having an opportunity to buy BTC for $52,000 on Jan. 29 might have made sense a couple of weeks ago, but not so much right now.

As the data above depicts, Deribit exchange remains the absolute leader with an 83% market share. Nevertheless, to understand how eventful this expiry could be, one must adjust data and compare both calls and put options near the current $32,000 BTC level.

It’s too early to panic

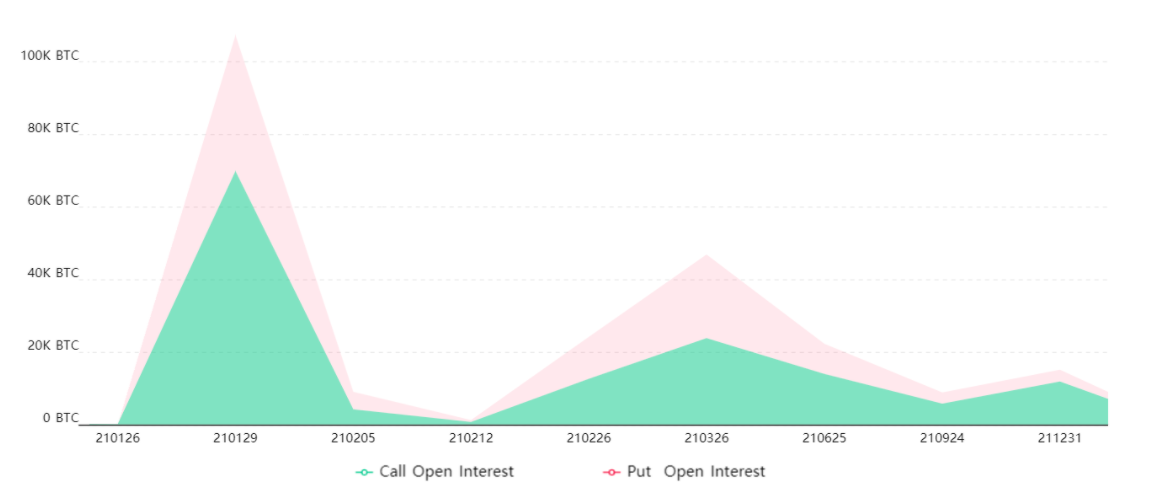

Most exchanges offer monthly expiries and some also hold weekly options for short-term contracts. Dec. 25, 2020, had the largest expiry on record as $2.4 billion worth of option contracts expired. This figure represented 31% of all open interest and showed how options are usually spread throughout the year.

Data from Bybt.com shows that Jan. 29 expiry calendar accounts for 107,000 BTC. This expiry date represents 45% of the aggregate options market open interest.

It is worth noting that not every option will trade at expiry as some of those strikes now sound unreasonable, especially considering there are less than five days left.

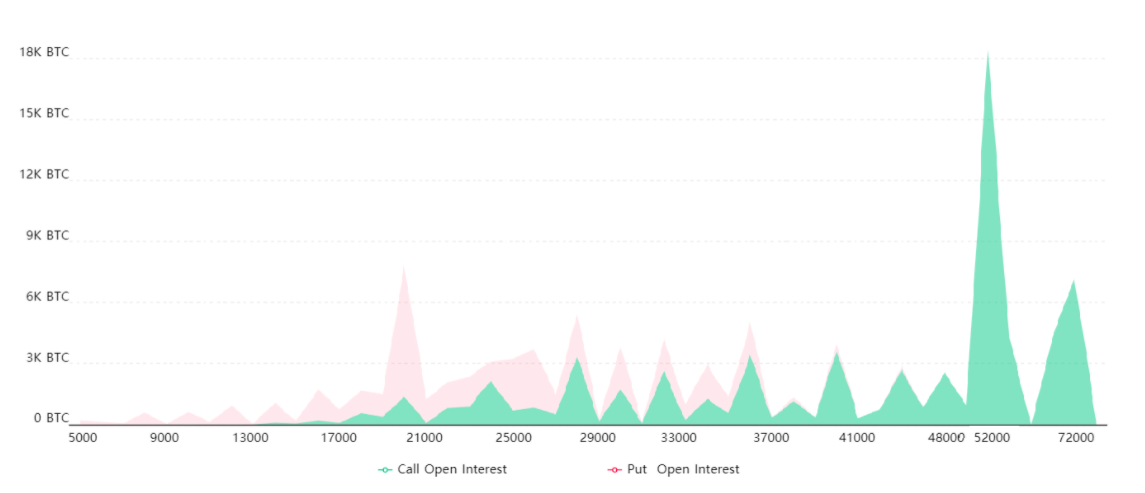

As Bitcoin marked its new $42,000 all-time high, some ultra bullish call options were traded but as BTC price adjusted, those short-term options became worthless.

Currently, over 68% of Jan. 29 call options at $40,000 and above should be disregarded for calculation. The same can be said for the bearish put options at $25,000 and below. These represent 76% of the open interest.

This data leaves an estimated $745 million worth of call options below $40,000 for the aggregate options expiry on Jan. 29. Meanwhile, the more bearish put options above $25,000 amount to $300 million. Therefore, the adjusted Jan. 29 open interest stands at $1.05 billion while holding a 0.40 put-to-call ratio.

Skew shows market makers are unwilling to take upside risk

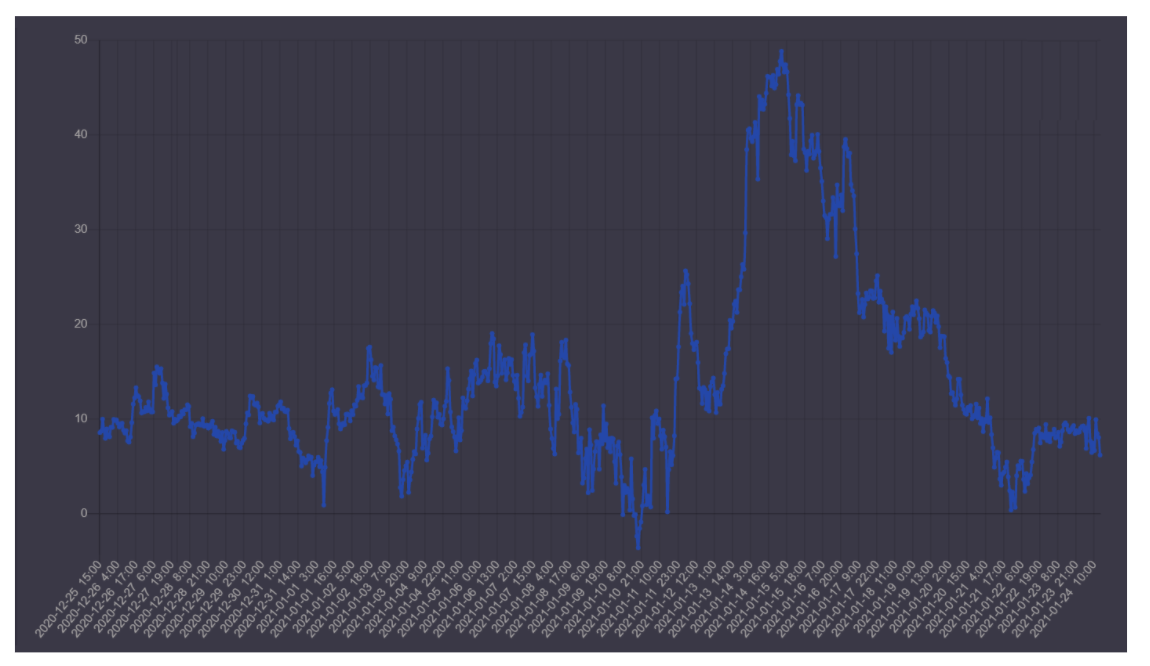

Analyzing open interest provides data from trades that have already passed, whereas the skew indicator monitors options in real-time. This gauge is even more relevant as BTC was trading below $23,500 just thirty days ago. Therefore, the open interest near that level does not indicate bearishness.

When analyzing options, the 30% to 20% delta skew is the single most relevant gauge. This indicator compares call (buy) and put (sell) options side-by-side.

A 10% delta skew indicates that call options are trading at a slight premium to the more bearish/neutral put options. On the other hand, a negative skew translates to a higher cost of downside protection and is a signal that traders are bearish.

According to the data shown above, the last time some bearish sentiment emerged was Jan. 10, when the Bitcoin price crashed by 15%. This move was followed by an extreme 30% to 20% delta skew as optimism reached 49, a level unseen over the previous past 12 months.

Whenever this indicator passes 20, it reflects fear of potential price upside from market makers and professionals, and is considered bullish. On the other hand, the current 0 to 10 range that held since Jan. 20 is deemed neutral.

While a $4 billion options expiry might be worrisome, nearly 74% of the options are already deemed worthless. Regarding the Jan. 29 expiry, bulls remain mainly in control due to its much larger adjusted open interest.

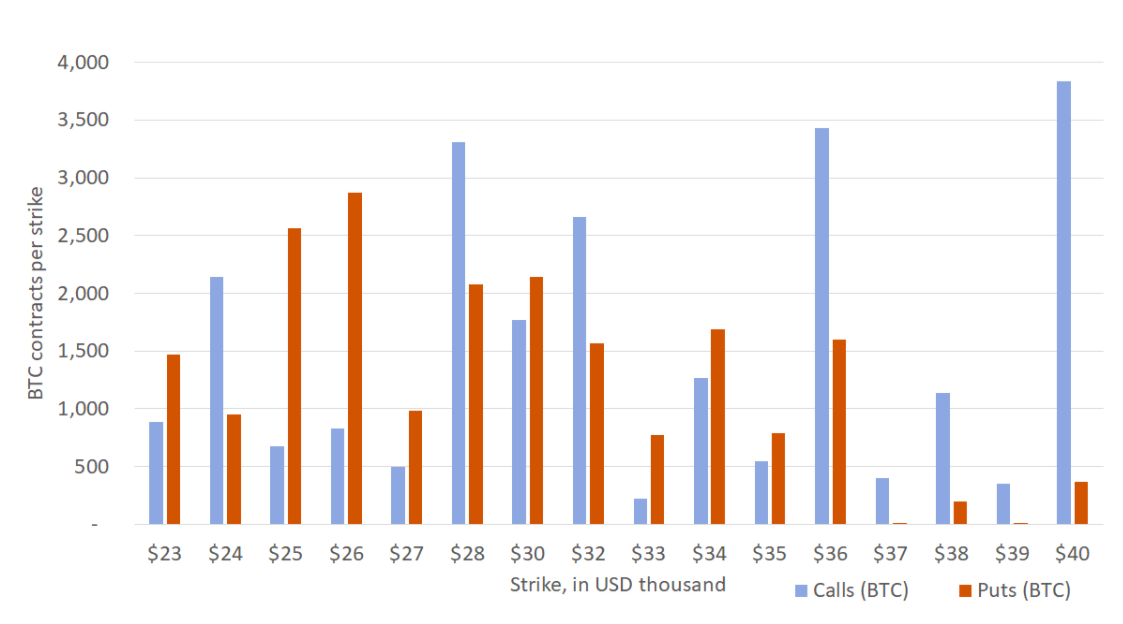

Bears are reasonably comfortable at $32,000

Despite bulls having an overall advantage, the more bearish put options dominate expiries between $33,000 and $35,000. Nevertheless, this 1,200 BTC contract advantage is more than offset by the 1,950 BTC contract imbalance favoring the call options from $28,000 to $32,000.

To conclude, as things currently stand, bulls seem in total control of Friday’s expiry, although incentives between $28,000 to $35,000 are reasonably balanced. Overall there’s not much to gain from either side to create additional volatility ahead of Jan. 29.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cryptox. Every investment and trading move involves risk. You should conduct your own research when making a decision.