The Securities and Exchange Commission (SEC) has brought down the hammer on crypto once again, announcing a $24 million penalty on blockchain company Block.one.

Yesterday brought equal measures of hope and despair for the cryptocurrency market. A new rating system for cryptocurrency classification sprung up, looking to bolster self-regulation efforts; at the same time, the SEC pounced on EOS‘ parent company, Block.one, for its supposedly unregistered ICO.

The company had tried to subvert the SEC’s security classification by merely avoiding registration. Nevertheless, according to Stephanie Avakian, Co-Director of the SEC’s Division of Enforcement, this didn’t stop the SEC from stepping in.

“A number of US investors participated in Block.one’s ICO… Companies that offer or sell securities to US investors must comply with the securities laws, irrespective of the industry they operate in or the labels they place on the investment products they offer.”

Within a statement of their own, Block.one neither admitted nor denied the SEC’s findings. Instead, they celebrated the fact that matter was settled, insinuating that the SEC would no longer be breathing down their necks.

“The settlement resolves all ongoing matters between Block.one and the SEC. The SEC has simultaneously granted Block.one an important waiver so that Block.one will not be subject to certain ongoing restrictions that would usually apply with settlements of this type.”

Chump’s Change for Block.one

According to the SEC press release, Block.one dug behind their humongous couch and drew out the fine, slapping it down on the agency’s desk without a second glance.

As mentioned by the regulatory body, during the EOS ICO, Block.one raised “the equivalent of several billion dollars.” In fact, that figure stands at approximately $4.1 billion; a fundraising effort that decimated any initial public offering (IPO) equivalent in the US that year. In comparison, the fine equates to a mere 0.58% of the firm’s ICO round. Funnily enough block.one spent roughly $6 million more than the $24 million fine on a domain name, earlier this year.

Let’s Show Them How It’s Done

Yesterday also saw a new attempt at cryptocurrency self-regulation, with several exchanges and cryptocurrency-based financial firms banding together to create the Crypto Ratings Council (CRC).

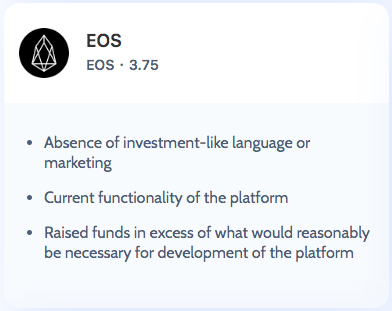

The council, which includes the likes of Coinbase, and Kraken, conceived a rating system to clarify the security status of a cryptocurrency. The system utilizes a “scalable, points-based rating system,” with ranks 1 through 5 denoting the increasing probability that a token could be a security. The initiative was created to challenge the Howey Test, an antiquated method of security classification currently used by the SEC.

Bitcoin came out on top, receiving a rank of 1, making it very unlikely to be considered a security. One of the main reasons for the low categorization was the fact that bitcoin lacked a token sale or ICO.

As for EOS’ classification, the CRC gave a fairly hefty 3.75, citing that the funds raised in the token offering surpassed what would be expected as “necessary for development.”

While the newly devised system remains purely advisory, it signifies a positive step towards self-governance and legitimacy within the cryptocurrency sector.

ETF Proposal By Canary Capital")

{kind=link}

{kind=link}

{kind=link}

{kind=link}