Human ingenuity finds a way around limitations. Sometimes these limitations are obstacles in the way of progress and creative thinking comes up with new paths. Sometimes these limitations are a lack of knowledge, and experimentation pushes the boundaries of the possible. And sometimes the limitations are rules, which a few believe don’t apply to them and which some take as a motivating challenge.

We see examples of the above every minute of our daily lives. It’s in the race to find a vaccine, the diplomatic posturing over privacy, the anguish of finding a way around unemployment, even your toddler’s determination to not eat the spinach. We also see it every day in crypto – it’s in the Twitter hack, the rush to develop better payments systems, the scramble to raise funds. The list goes on.

You’re reading Crypto Long & Short, a newsletter that looks closely at the forces driving cryptocurrency markets. Authored by CryptoX’s head of research, Noelle Acheson, it goes out every Sunday and offers a recap of the week – with insights and analysis – from a professional investor’s point of view. You can subscribe here.

Last week threw up a couple of examples that not only exhibit increasingly frequent manipulations of protocol rules, they also highlight one of crypto’s core value propositions.

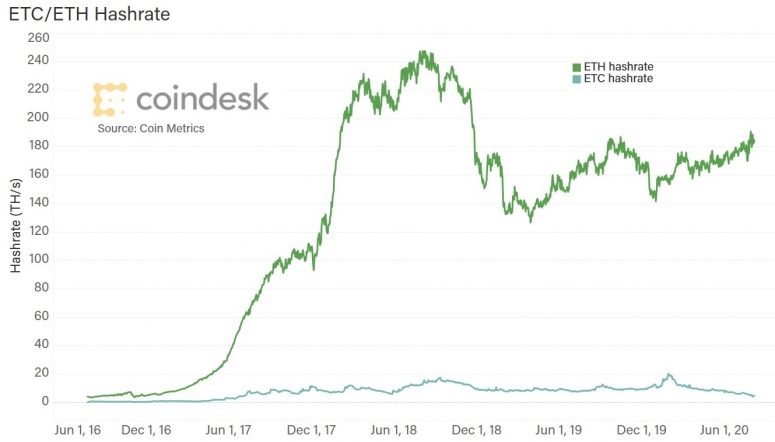

Ethereum Classic is the original Ethereum blockchain maintained by stakeholders that refused to jump over to the fork that corrected for The DAO hack in 2016. Over the past few days it has suffered not one, but two 51% attacks.

A 51% attack happens when enough mining computing power (also known as hashpower) colludes to alter previously processed blocks and determine new ones, allowing attackers to block some transactions and reverse others. In a 51% attack, malicious miners could create a competing blockchain that allows the same coins to be spent twice.

This maneuver is relatively frequent in smaller blockchains such as Ethereum Classic (ETC), which has a market cap of approximately $830 million at time of writing. Ethereum’s (ETH) market cap, for comparison, is currently around $44 billion. The attacks are usually brief, and then business carries on as usual. But two in the space of one week has prompted some commentators to question the blockchain’s survival.

The amounts lost are not inconsiderable. In the first attack, the malicious miner(s) managed to double-spend a little over 800,000 ETC (about $5.6 million) after paying about $204,000 to acquire the necessary hash power. In the second attack, the double-spend was at least $1.6 million.

This is more than a lesson for investors to be wary of smaller proof-of-work blockchains. It also puts to rest the notion that open-source software, such as the Bitcoin (BTC) blockchain, is vulnerable to copies. And it is a clear example of why network security is a fundamental part of an asset’s value.

Size matters

In a recent essay, Lex Sokolin hinted at the potential power of large open-source networks, and the capacity for innovative economies to build competitive moats. This can apply to multinational platforms, as well as to individual blockchains. “Finally,” he wrote, “we can see where copying a product without having an existing commercial community doesn’t have any positive effect. Take, for example, the forking of Bitcoin into Bitcoin Cash (BCH), or any other 50 or so clones of the coin. Or alternately, even the more contested forks like Ethereum Classic do not really compete for the dominant spot given the much smaller market presence.”

In other words, copies can be made, and Bitcoin/Ethereum forks can be spun up relatively easily. Some have even suggested that this could weaken Bitcoin’s hard cap value proposition – the limit isn’t really 21 million, the reasoning goes, if other networks based on the same blockchain can choose the limit they want. But this unfounded concern overlooks the value of the community behind a network. However convinced you may be that bitcoin cash (for example) has superior characteristics, people prefer to trade and transact with bitcoin because that is where the volume is.

You can copy an open-source technology. But what gives a technology value is the community and network support from users.

Security in numbers

In the case of crypto assets, the community and network support are more than just transaction volume generators. They have a material influence on the network’s development and security, which further enhances the asset’s value.

The greater the transaction volume of a blockchain, the more interesting it is for miners, who earn a fee on transactions. And the greater the potential demand for an asset, the greater the value of the rewards miners earn from processing blocks. So, a network with strong prospects for growth in volume and value will attract a wider pool of miners.

A wider pool of miners makes it much harder for any one bad actor to engineer a 51% attack. In the case of Bitcoin, the computing power needed to successfully manipulate a meaningful number of blocks would be prohibitively expensive. For smaller blockchains, it’s relatively cheap.

This is why it is important to keep an eye on the health of the Bitcoin mining industry. It is currently struggling, and not just because the recent halving reduced miners’ income in BTC terms by almost 50%. The activity is still concentrated in China, where miners are grappling with overcapacity and a much longer wait to recoup initial investment. Internal troubles at one of the industry’s largest hardware suppliers are not helping.

Miners dropping out would weaken Bitcoin’s security, which could negatively affect its value, which could cause more miners to drop out, and so on in an unfortunate spiral. But more miners joining the network could increase security and value, and encourage more participation, further boosting the value.

A glitch in this pattern is the regularly scheduled halving event, which reduces the block subsidy by 50%. Unless the value of BTC and/or transaction fees rise to offset the difference, mining will be less profitable for some and unprofitable for many, which could negatively impact security. Some have argued that as miners’ rewards become more dependent on fees, the network will be more vulnerable to 51% attacks.

So far, Bitcoin’s hashrate – a good proxy for the health of the mining industry – is stronger than ever, in spite of the reduced income, which should reassure investors that a 51% attack is not a significant risk for market’s largest network.

Ethereum’s current hashrate is also robust, unlike that of Ethereum Classic.

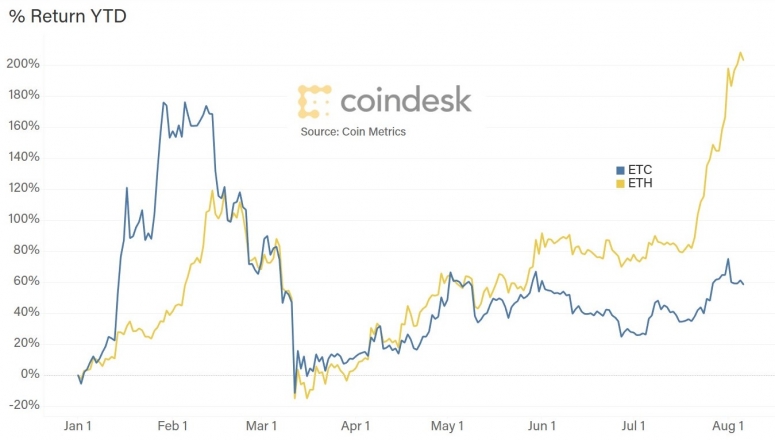

One mystery is why ETC’s price has not plunged as a result of the hacks. Over the week, it has fallen 10%, a paltry amount given the attention these hacks are getting, not to mention the blow to investor confidence. A possible explanation could be that the likelihood of 51% attacks is already priced in. In other words, ETC already carries a significant discount for its lack of security. Its performance since the beginning of 2019 is less than one fifth that of its much larger sibling. And a decline of 10% in a week when the ETH price rose by almost 15% is telling.

Ethereum’s planned move away from a proof-of-work blockchain will change its security equation, removing the threat to mining but no doubt introducing other possible attack vectors. However, attacks can make a network stronger, if and only if there is a large and active community of stakeholders willing to invest resources into development, growth and preventing future attacks.

In this together

An active community creates value, which grows the active community, in a virtuous cycle. In an essay for CryptoX this week, Nic Carter points out that Bitcoin’s patronage system signals one of the network’s strongest advantages: investment in and by its stakeholders. Also this week, OKCoin awarded its largest individual grant so far to Bitcoin’s second-most prolific contributor to the core code.

These “patronages” have at their root the recognition that a strong network benefits all participants. This is difficult to replicate in smaller networks, where issued coins tend to be held in concentrated pockets and the businesses that could profit are few. It is even more difficult to replicate in traditional open-source technologies, where network effects are harvested by private businesses and profits flow towards size.

In crypto, the network effects are enjoyed by the whole community, not just for-profit businesses.

The difference between crypto and other technologies is that Bitcoin, Ethereum and others are more than technology networks, they are also value networks. And what gives these networks their value?

That’s what 51% attacks on smaller networks teaches us. That it’s not the technology, and it’s not even the alleged revolutionary potential of some of the functionalities. It’s the community that gives value. That comprises the body of work so far, the energy and time invested every day, the creativity and the intellect, the conviction and the sense that what everyone is working on is bigger than any one business or individual.

Attacks will happen, and networks and people will come and go. But an immense body of people working together to build networks that are not controlled by anyone and that distribute value in unusual and sometimes intangible ways – that is here to stay. Because people have throughout history shown that resilience comes from collective effort supporting powerful ideas.

Anyone know what’s going on yet?

As explosions wreak heartbreaking damage to an area that can ill afford it, as geopolitical tensions muscle their way into the use of social media and communication platforms, and with no agreement in sight on a fifth coronavirus U.S. relief bill, markets seem to be getting increasingly nervous about the international balance of capital flows.

Gold breezing past $2,000 for the first time ever is itself news, as well as a symptom of growing market unease. Tentatively encouraging employment figures are welcome, but have not soothed the nervous vibe, as concerns about inflation and the dollar’s role as a global reserve currency seem to be gathering steam.

In bitcoin, could it be that volatility is back? After weeks of trading within a relatively narrow band, bitcoin broke out last weekend, climbing 5% to almost $12,000, only to sharply drop 8% in a matter of minutes. Sigh, it’s starting to feel almost normal again.

Bitcoin’s recent rally has given it a strong lead over other asset groups in terms of year-to-date performance, with even gold left far behind. And even reasonable commentators are starting to talk about a “bull market.”

CHAIN LINKS

Goldman Sachs has appointed a new head of digital assets, and is boosting the team. TAKEAWAY: Matthew McDermott has taken over from Justin Schmidt, and has brought on board Oli Harris, former head of digital assets for JPMorgan. That does not mean that we’ll see a Goldman Sachs crypto trading desk in the near future (although it isn’t ruled out) – the short-term focus seems to be on the impact that blockchain technologies can have on capital markets, with a Goldman Sachs stablecoin possibly on the cards. This in itself is exciting, as few other legacy institutions have the necessary clout to give capital markets a meaningful nudge along the road to greater efficiency.

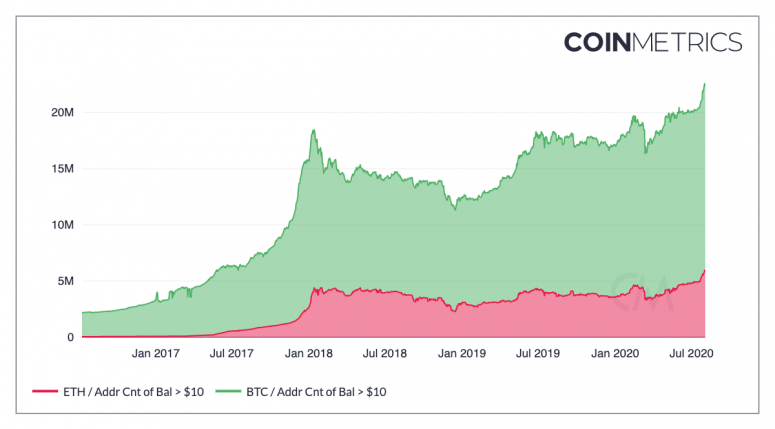

Coin Metrics points out that the number of addresses on the bitcoin blockchain that hold more than $10 worth of BTC is at its highest level ever, 14% higher than at the peak of the 2017 bubble. TAKEAWAY: Using the dollar-based price may be intuitively easier to visualize, but it can also distort the growth. If the BTC price rises, the number of addresses with a certain dollar balance will also rise, even if holders do not buy more bitcoin. The number is considerably higher than at the end of 2017, however, which is notable, since the BTC price was much higher then. In other words, there has been strong growth in the number of holders of small amounts of bitcoin over the past two-and-a-half years.

This chart using data from Glassnode shows that the number of unique addresses holding less than 1 BTC has easily outstripped larger holdings, confirming a dispersion of ownership – more small savers are accumulating positions.

The conversation is getting louder. I’m surprised by how fast bitcoin is making its way into “mainstream” financial discourse (whatever that means in these strange times, of course). First, we had Barstool Sports’ Dave Portnoy (@stoolpresidente) start to put bitcoin in front of his 1.7 million followers. Then we had “Rich Dad” himself (@theRealKiyosaki) recommend that his 1.4 million followers buy bitcoin “and get richer.” And we also saw publicly traded business intelligence company MicroStrategy casually say in a recent earnings call that it was thinking of investing $250 million of its excess cash into “alternative assets” such as, you guessed it, bitcoin.

While we continue to receive news of crypto funds closing down, such as Neural Capital, which lost half its money since launching in 2017, there are also some that are doing well. TAKEAWAY: Electric Capital closed its second venture fund at $110 million, more than three times the raise for its first fund just two years ago. Traders and investors watching the spot and derivative markets for signs of institutional-sized volume are missing indicators that institutional capital is already here. 90% of Electric’s raise was from institutions, including university endowments.

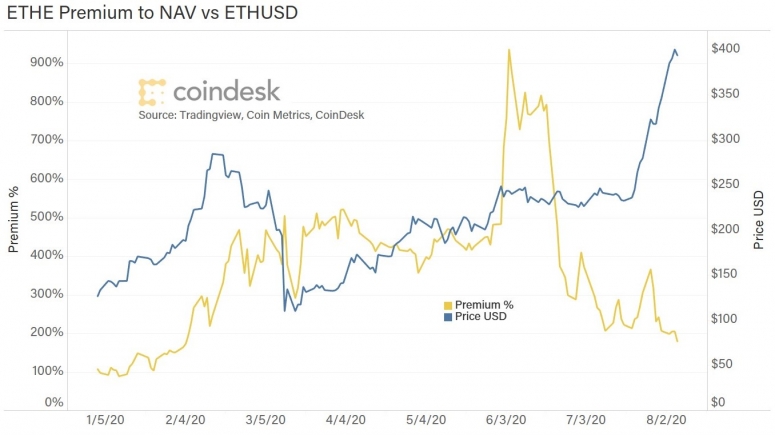

Grayscale Investments* has publicly filed a Form 10 Registration Statement with the U.S. Securities and Exchange Commission in order to designate Grayscale Ethereum Trust as an SEC reporting company. TAKEAWAY: This would reduce the statutory holding period from 12 months to six (starting 90 days after designation, and contingent on other Securities Act requirements being satisfied), which could enhance the appeal to a broader range of investors. Many active investors are likely to prefer the shorter lock-up, and some institutions are unable to hold assets that are not registered with the SEC. Also, greater liquidity could reduce the premium that retail investors pay – this has been falling anyway, from over 900% in early June to just (?!) 180% at time of writing. (*Grayscale Investments is owned by DCG, also parent of CryptoX.)

Podcast episodes worth listening to: