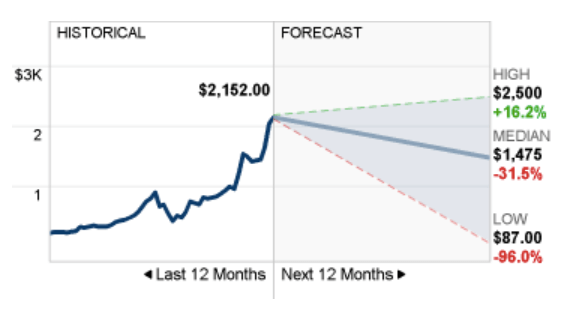

- Jefferies has upgraded its 12-month target for Tesla to $2,500, only a couple of months after upgrading this target from $650 to $1,200.

- The upgrade indicates that Wall Street is increasingly warming to the carmaker, although opinion still remains very mixed.

- Under normal circumstances, the Tesla bubble should be expected to burst, but there are few attractive investment opportunities outside of high-growth stocks.

Financial analysts Jefferies has more than doubled its price target for Tesla (NASDAQ:TSLA) to $2,500. It settled on its previous target of $1,200 as recently as June, showing just how quickly Wall Street is warming up to the electric carmaker.

Jefferies’ target of $2,500 is now the highest on Wall Street, which remains split on estimates for the Elon Musk-founded manufacturer. The lowest 12-month target is the $87 of GLJ Research’s Gordon Johnson, who said on Monday that the Tesla rally is “detached from reality”.

Jefferies had lowered its Tesla target to $650 in April while forecasting that it could rise by 35% by the end of 2020. Given that Tesla has surged by 317% since this April prediction, it’s hard to trust the wisdom of Jefferies new estimate. But in an economic environment where an expanding money supply has nowhere else to go but stocks, all bets are still off.

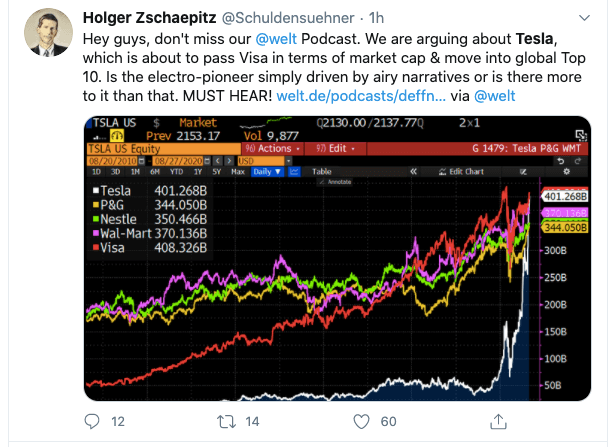

Tesla Heading For $2,500, Says Jefferies

Barely a couple of months after predicting that Tesla would reach $1,200, Jefferies has now hit on a 12-month target of $2,500 for the carmaker. According to analyst Philippe Houchois, this optimistic benchmark is supported by Tesla’s recent financial performance and its head start in automotive software and EV batteries.

Tesla has executed much better than anybody expected through the course of 2019, but also through the pandemic. I think all those things together will continue to support the valuation.

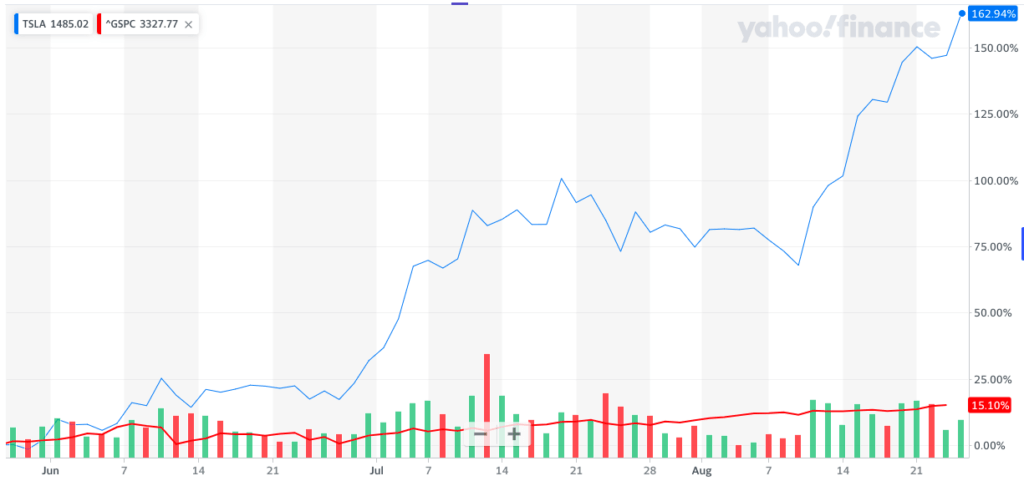

Tesla closed yesterday at $2,153. This represents a 6% one-day rise, a 52% one-month rise, and a 163% three-month rise.

The stock needs to rise by “only” another 16% or so to match $2,500. It is due for a five-for-one split on August 31, so whatever valuation it has on this date will be divided by five.

Analysts Don’t Have A Clue

It would be easy to mock Jefferies for so rapidly and drastically changing its targets. But its speedy updates suggest that, despite initially arousing plenty of skepticism, Tesla is gradually winning Wall Street over.

Jefferies analyst Houchois admits that the firm doesn’t really know what’s happening with the company.

We cannot pretend to understand the magnitude and speed of share price moves.

Other analysts aren’t quite as exuberant. The median target of 31 analysts providing 12-month forecasts is currently $1,475. Wedbush’s Dan Ives now has a “bull case” target of $3,500, up from $2,500 barely a week ago.

The lowest target is $87, from GLJ Research’s Gordon Johnson.

Johnson told Yahoo Finance’s the First Trade that Tesla remains tiny compared to other carmakers. He also noted that the company would still be making a loss if it weren’t for credit revenue sales (which involve selling environmental credits to other carmakers). These were worth four times as much as Tesla’s net profit of $104m in Q2 2020.

That’s essentially taxpayer incentives that they’re getting for selling credit revenues to other car companies. The problem is all of those car companies are now selling electric cars, and Tesla is guiding their credit revenue sales to be down 50% in the back half of this year.

Tesla may very well be a stock to avoid under normal circumstances. But with interest rates low, the wider economy stagnating and QE in full effect, it offers the kind of growth narrative that’s lacking from more conservative sources.

This is why it has been shooting upwards this year. And it’s likely to continue surging for as long as the “real” economy has little to offer.

Disclaimer: The author holds no positions in the securities mentioned in this article.

Traders Predict $28,000, Crypto Alts Solana (SOL), XRP, Cardano (ADA) Surge")