Nonfungible tokens (NFTs) are constantly in the news. NFT platforms are springing up like mushrooms and champions are emerging, such as OpenSea. It is a real platform economy that is emerging, like those in which YouTube or Booking.com gained a foothold. But it is a very young economy — one that is struggling to understand the legal issues that apply to it.

Regulators are starting to take an interest in the subject, and there is risk of a backlash if the industry does not regulate itself quickly. And, as always, the first blows are expected east of the Atlantic.

In this first article devoted to the legal framework of NFTs, we will focus on the application of the digital asset regime and financial law to NFTs in France. In a second article, we will come back to the issues of liability and copyright.

Related: Nonfungible tokens from a legal perspective

A digital asset?

In France, the definition of digital assets includes two types of tokens. On the one hand are utility tokens, i.e., all intangible assets representing, in digital form, one or more rights, which can be issued, recorded, stored or transferred by means of a shared electronic recording device allowing the owner of the asset in question to be identified, directly or indirectly.

NFTs are intangible assets that can be issued, recorded, retained or transferred through shared electronic records.

On the other hand are payment tokens, i.e., any digital representation of value that is not issued or guaranteed by a central bank or public authority, is not necessarily linked to a legal tender, and does not have the legal status of money, but is accepted by natural and legal persons as a medium of exchange that can be transferred, stored or exchanged electronically.

Is an NFT a digital asset under French law?

An NFT is acquired to obtain a property right, but it can also be acquired to claim the performance of one or more services related to that NFT.

Furthermore, an NFT can be seen as a digital representation of value that is not issued or guaranteed by a central bank or public authority, that is not necessarily linked to a legal tender and does not have the legal status of money, and that can be stored or exchanged by electronic means. It follows that NFTs could be classified as digital assets, either as a token of use, a token of payment, or both.

The consequence of classifying NFTs as digital assets would be twofold.

Registration as a virtual asset service provider

If the platform issuing NFTs implements, in addition to its primary market, a secondary market on which users would benefit from: 1) a digital asset storage service or access to digital assets for the benefit of a third party in order to hold, store or transfer these digital assets, and/or 2) a service of purchase or sale of digital assets in legal tender, and/or 3) a service of exchange of digital assets for other digital assets, and/or 4) the operation of a platform of trading of digital assets, then a compulsory registration as a digital asset service provider with France’s financial regulator, the Autorité des Marchés Financiers (AMF), is required.

In addition, clients must be identified through a Know Your Customer. Our analysis is supported by the fact that NFTs are referred to as “crypto-assets” by the proposed European regulation, “Markets in Crypto-assets” (MiCA).

Related: How should DeFi be regulated? A European approach to decentralization

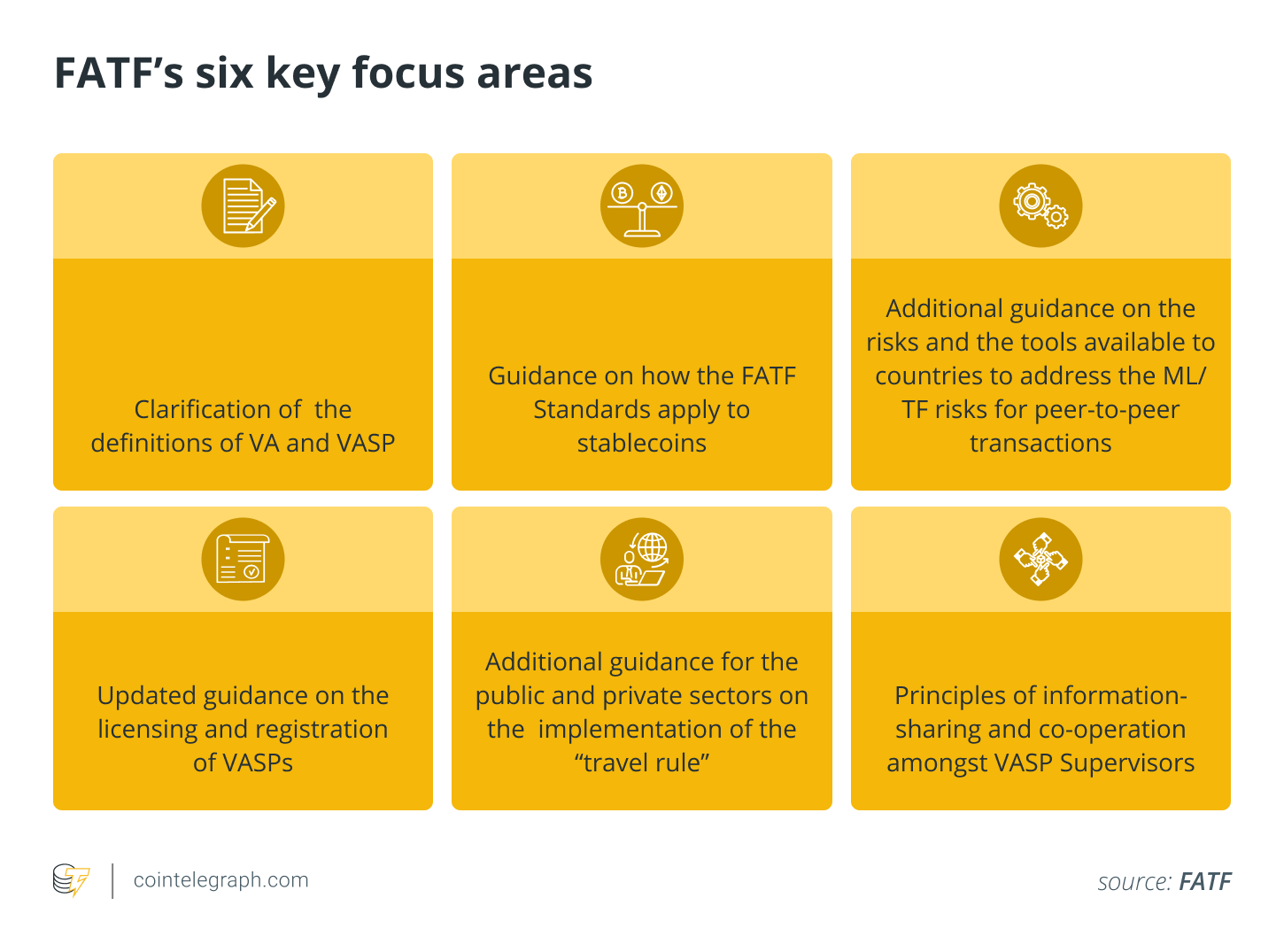

The Financial Action Task Force (FATF) has also issued an opinion on the assimilation of NFTs into “digital assets” in its famous recommendation of October 2021. It states that NFTs are “generally not considered [virtual assets].”

However, like its approach to DeFi, FATF emphasizes that regulators should “consider the nature of the NFT and its function in practice, not the terminology or marketing terms used.” In particular, FATF argues that NFTs that “are used for payment or investment purposes” can be virtual assets.

Related: FATF guidance on virtual assets: NFTs win, DeFi loses, rest remains unchanged

Although the directive does not define “for investment purposes,” FATF likely intends to capture those who purchase NFTs with the intent to resell them later for a profit. While many buyers purchase NFTs because of their connection to the artist or work, a large portion of the industry buys them because of their potential to increase in value. In other words, many NFTs could qualify as digital assets to follow this interpretation.

Application of the ICO regime?

As soon as there is a public offering of digital assets (to more than 150 potential buyers) in France, the French ICO regime applies. The issuer is then subject to the following rules: The “simple” advertising of the token offering is allowed, but any canvassing would be prohibited as well as any “quasi canvassing,” except if the issuer has obtained the AMF visa.

This is a delicate point here because the NFT issuer could not “invite” French residents to register on its site without violating the law. It would then be required to never target “French” groups or communities.

However, we do not believe that the ICO regime is applicable to NFTs, because this regime is designed to regulate a fundraising operation and protect the investor. Certain provisions of the law are incompatible with an NFT offer (i.e., offer limited to 6 months, sequestration of funds during the ICO, etc.).

This is the spirit of the proposed MiCA regulation, which considers NFTs as digital assets by default, but excludes them from certain obligations specific to ICOs (publication and notification of a white paper).

Anti-money laundering obligations and KYC?

We have already noted the risk of qualifying as a virtual asset service provider (VASP), which would entail a KYC obligation (from 1 euro of transaction). In addition, persons acting as intermediaries in the art trade, including when it is carried out by art galleries, when the value of the transaction is equal to or greater than 10,000 euros, are subject to an obligation to apply due diligence measures based on the assessment of the risks presented by their activities in terms of money laundering and terrorist financing.

Related: NFTs and compliance: Why we need to be having this conversation

In short, all NFT platforms, which are linked to digital works of art, should implement KYC procedures even if they do not qualify as digital assets, which today is far from being the case.

In the United States?

We know that the approach in the United States is different than in Europe because the U.S. Securities and Exchange Commission (by applying the famous “Howey Test”) qualifies tokens that would be seen as digital assets in Europe, as securities.

The risk of the SEC classifying tokens as “securities” is therefore significant. The SEC has not yet come to a firm conclusion on the issue, but there have already been suggestions that some NFTs could be qualified as securities, especially when they are sold in a fractional manner.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cryptox.

Thibault Verbiest, an attorney in Paris and Brussels since 1993, is a partner with Metalaw, where he heads the department dedicated to fintech, digital banking and crypto finance. He is the co-author of several books, including the first book on blockchain in French. He acts as an expert with the European Blockchain Observatory and Forum and the World Bank. Thibault is also an entrepreneur, as he co-founded CopyrightCoins and Parabolic Digital. In 2020, he became chairman of the IOUR Foundation, a public utility foundation aimed at promoting the adoption of a new internet, merging TCP/IP and blockchain.