U.S. regulators and law-enforcement officials brought charges on Thursday against BitMEX, a Seychelles-based cryptocurrency exchange that has grown in recent years to be one of the industry’s biggest players.

According to the U.S. Commodity Futures Trading Commission, prosecutors accused BitMEX of facilitating unregistered trading and other violations, including “conducting significant aspects of its business from the U.S. and accepting orders and funds from U.S. customers,” as reported by CryptoX’s Nikhilesh De.

The news dominated cryptocurrency news headlines and sent traders and analysts scrambling to assess the damage and implications. Some 23,000 bitcoin were apparently withdrawn from BitMEX addresses in a single hour, the cryptocurrency-markets data firm Glassnode tweeted early Friday, citing blockchain data.

BitMEX, led by CEO Arthur Hayes, said it intends to defend against the allegations “vigorously” adding that the trading platform was operating normally and that all funds were safe.

Bitcoin prices tumbled after the announcement, as illustrated by CryptoX’s Daniel Cawrey in an hourly price chart:

Cryptocurrency traders are conditioned to expect volatility whenever there’s major news involving one of the biggest industry exchanges, but despite the quick drop, prices quickly stabilized, as reported by CryptoX’s Zack Voell.

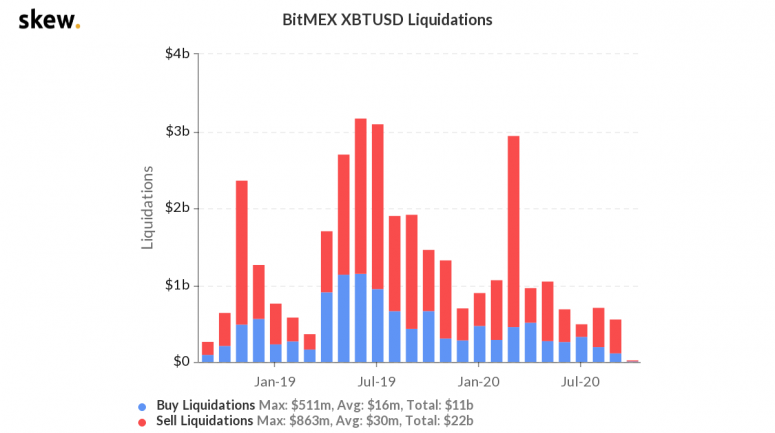

BitMEX is a well-known player in the constellation of global cryptocurrency exchanges, partly because it was a pioneer, in 2016, of a new product called the “perpetual bitcoin leveraged swap.” At the time, few traders in nascent digital-asset markets could have anticipated what a major impact the obscure roll-out would have on the industry.

But the instrument, which made it easy for customers to trade the equivalent of $100 of bitcoin for every $1 down, proved hugely popular and successful among risk-hungry traders, vaulting BitMEX into the top ranks of the world’s biggest cryptocurrency exchanges.

Even so, the perpetual swaps were infamous for exacerbating price swings: It’s a well-known trope among bitcoin traders that every time the market tilts one way or another, BitMEX customers’ thinly capitalized positions get liquidated in a series of rapid margin calls, exacerbating price swings that reverberated to other exchanges.

Such episodes are so notorious that crypto traders even have a slang verb for the phenomenon: to get “rekt,” with websites and even Twitter accounts devoted to tracking their magnitude and frequency.

If BitMEX’s role in the markets were to diminish, that might mean fewer volatility-inducing liquidations.

“Long term, it’s so much better for the spot market,” Steve Ehrlich, CEO of Voyager Digital, an online cryptocurrency trading platform, told First Mover.

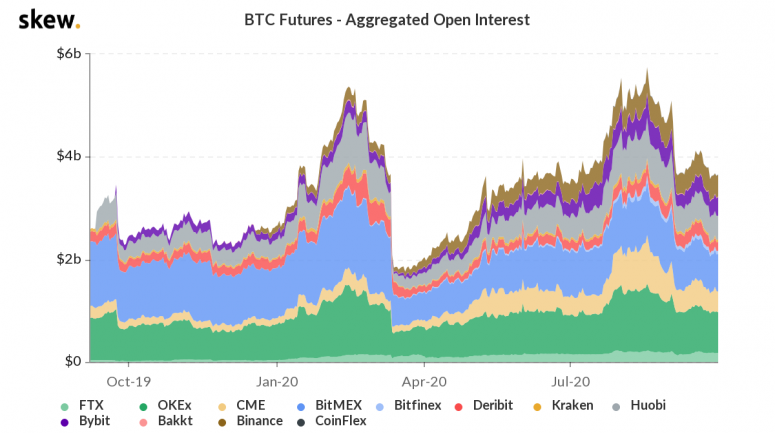

Industry executives were quick to point out that some traders had apparently been shifting their allegiances recently to rival exchanges that had copied BitMEX’s “100x” bitcoin derivatives contracts.

“Two years ago, this would have been catastrophic, because BitMEX was such a huge percentage of everybody who’s playing leveraged trading,” David Weisberger, co-founder and CEO of CoinRoutes Inc., told CryptoX’s Muyao Shen in a phone interview. “Now, there are quite a few alternatives to BitMEX and several of them have always been more stringent about trading or not allowing U.S. clients to trade on those platforms.”

CryptoX’s William Foxley reported that the BitMEX news reverberated in the fast-growing blockchain-based sector of “decentralized finance,” or DeFi, where programmers are developing semi-automated platforms for lending and trading.

The systems are often cast as “uncensorable” since they mainly exist within strings of programming encoded atop the Ethereum blockchain network. The question is whether they still might be subject to the laws of various jurisdictions, since they are, ultimately the craft of “real, live humans.”

Centralized exchanges such as BitMEX as “opaque platforms that can easily facilitate money laundering,” Robert Leshner, founder of the DeFi lender Compound, told Foxley. “By contrast, DeFi done right is a breath of fresh air – complete transparency, accountability, tamper-resistance and self-custody.”

Cryptocurrency industry regulations are still evolving, and the rulemakers are always a few or myriad steps behind. But they do sometimes crack down, and it’s probably not a coincidence that often they take aim at the most threatening upstarts, those that attempt to change the rules of the game.

Bitcoin Watch

Bitcoin has come under pressure in the past 24 hours, seemingly due to the BitMEX controversy and risk-off moves in traditional markets.

On Thursday, the U.S. Commodity Futures Trading Commission (CFTC) and federal prosecutors announced they’re charging BitMEX for failing to implement anti-money-laundering procedures and operating an unregistered trading platform.

Further, President Trump announced early Friday he and his wife had tested positive for coronavirus and were going into self-quarantine, ratcheting up pre-election uncertainty and sending global equities lower.

Bitcoin has declined from $10,900 to $10,400 in the past 24 hours. The daily chart now shows the cryptocurrency is stuck in a narrowing price range.

A triangle breakdown would signal a continuation of the sell-off from August’s high above $12,400 and expose the 200-day average support at $9,400.

Alternatively, a breakout could invite stronger chart-driven buying pressure.

Token Watch

Ethereum (ETH): Ethereum developers will take a second whack at a final Ethereum 2.0 “dress rehearsal” after the first, Spadina, failed due to “critical peering issues.”

What’s Hot

Analogs

The latest on the economy and traditional finance

Tweet of the Day