- The U.S. housing market recovery has been nothing short of extraordinary.

- There’s still one problem, though, and it threatens the pace of the real estate sector rebound.

- The mortgage market has a credit crisis, and it’s only getting worse.

Given the headwinds faced by the U.S. economy, it would be hard to imagine a stronger housing market recovery than the one we’re currently witnessing.

The Housing Market Recovery Is Extraordinary in Every Way But One

Homebuying demand remains as strong as ever – or at least since the housing bubble. Mortgage applications for home purchases have climbed for eight consecutive weeks, and purchase activity is now 13% higher than at the same point in 2019.

With mortgage rates plumbing new lows this week, there’s no reason to think demand will collapse anytime soon.

And after-the-purchase data is beginning to look up too. Housing market “bailout” programs have shrunk for two consecutive weeks. A net 112,000 mortgages have exited forbearance since peaking during the week of May 22.

To be sure, it’s concerning that 4.66 million borrowers – or 8.8% of all active mortgages – remain in forbearance. But many of these borrowers are still making payments, and the consensus is that expanded forbearance hasn’t transformed into the crisis mortgage servicers initially warned it would be.

All of this is unquestionably good news. But there’s still one big threat hanging over the U.S. housing market. The mortgage industry has a credit crisis, and the latest data reveal that it’s only getting worse.

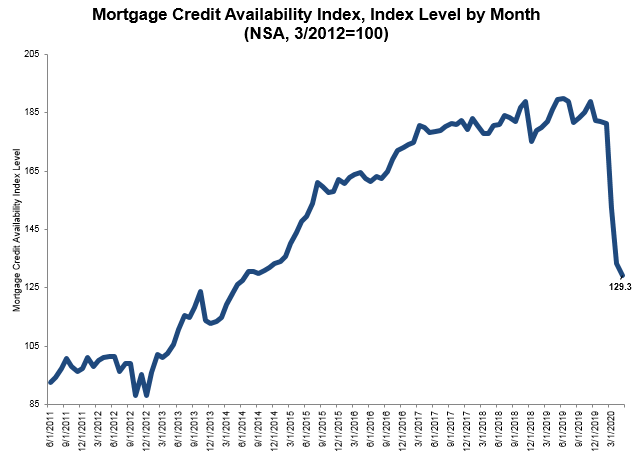

Mortgage Industry Credit Crunch Gets Worse

According to statistics published by the Mortgage Bankers Association (MBA) this week, available mortgage credit declined 3.1% in May, which indicates that mortgage providers are tightening their lending standards.

It was the third straight monthly decline for the Mortgage Credit Availability Index (MCAI), which closed the month at its lowest level since June 2014.

Joel Kan, MBA’s associate vice president of economic and industry forecasting, commented:

Mortgage lenders in May responded accordingly to the increased risk and uncertainty in the economy. Credit availability continued to decline, with MBA’s overall index now at its lowest level since June 2014.

There was a reduction in supply across all loan types, driven by further pullback in investors’ appetites for loan programs with low credit scores and high LTVs. Credit tightening was observed at both ends of the market, with less availability of low downpayment programs designed for first-time homebuyers, as well as for conforming and non-conforming jumbo loans.

The silver lining is that May’s 3.1% decline was much smaller than the ones the MCAI endured in March (16.1%) and April (12.2%).

But the unavoidable upshot is that this indicates that conditions have only continued to worsen since the Wall Street Journal published a worrisome report on the impact that the mortgage industry credit crunch could have, not just on the housing market, but on the entire U.S. economy.

Beyond making it more difficult for more Americans – especially millennials – to tap into one of the economy’s most basic wealth-building tools, tight lending standards are making it difficult for current homeowners to refinance while interest rates are at record lows.

With wages under pressure, refinancing would free up cash in many household budgets, indirectly providing a boost to consumer spending. But not if homeowners can’t get approved for a new loan.

The most concerning statistic in the Wall Street Journal’s report – which was published in late May – came from the Urban Institute think tank, which estimated that two out of three loans approved in 2019 would be denied by at least one major lender in today’s environment.

Glimmers of Hope for Housing Market Bulls

If there’s any good news on this front, it’s that mortgage lenders appear to be hiring as aggressively as they were before the pandemic. This provides a glimmer of hope that mortgage credit availability is going to bottom out soon.

And to that end, refinance activity did improve in the MBA’s latest mortgage applications report, which tracked data for the week ending June 5. It was the first weekly gain in refinance application volume in nearly two months.

This article was edited by Sam Bourgi for CCN.com. If you find any factual, spelling, grammatical errors or spot a breach of the Code of Ethics of the Norwegian Press, please leave a comment below this article. The comment will not be published, but we will act swiftly to investigate any errors claimed by our readers.