Welcome to this week’s Money Reimagined, coming to you two days into a new U.S. presidency.

Already, with various executive orders and a host of cabinet and agency nominee names emerging, President Joe Biden has fostered the palpable sense of a slate being cleaned.

As for what it means for crypto, the turnover in the White House gave Sheila Warren and me reason to invite Kristin Smith of the Blockchain Association and Amy Kim of the Digital Chamber of Commerce onto our weekly podcast. We discussed the outlook for regulation under the Biden administration. Check out the episode. But first, read the newsletter, which starts with an open letter to the new U.S. president.

Is Biden ready for a new world of money?

Dear President Biden,

Congratulations on an inspiring inauguration.

The stirring speeches, uplifting poems and dazzling fireworks conveyed a real sense of purpose and hope. But now they’re over. Time to get to work.

Let’s first check the dashboard:

- COVID-19 deaths: 408,000

- Unemployed Americans: 10 million

- Fiscal deficit: $3.3 trillion

- Government debt to GDP: 98.2%

You most urgently need to tackle the first two items. But that will only push the third and fourth numbers much, much higher.

What’s more, the dashboard is dangerously simplistic. The problem is not the U.S. government balance sheet per se, but the global account. In November, the Institute of International Finance forecast that world public debt would hit $277 trillion by year’s end, or 365% of world GDP. As for advanced economies, their aggregate debt was at 432% of GDP in the third quarter.

The task at hand: to get the international community to jointly get those numbers into a sustainable state and avoid a 1930s-style global depression.

Ignore the deficit hawks telling you fiscal austerity is the answer. You can’t ask an exhausted public to bear the cost of making bankers and hedge fund managers whole unless you want a violent insurrection far bigger than the one on Jan. 6.

Yet, it’s impossible to foresee the degree of economic growth needed to repay those debts.

The only way out is through synchronized debt monetization. That means addressing the elephant in the room: overhauling the global financial system in which the U.S. dollar is king. It means recreating that system around digital currencies.

Coordinated action

Why must this be an international solution? Well, let’s first look at how a unilateral fix would play out, if it were actually possible:

- The Federal Reserve would go full MMT (Modern Monetary Theory) printing dollars with abandon.

- More circulating dollars equals higher nominal U.S. tax collection.

- Voilà! The fixed-value debt is easily paid off.

- Meanwhile, the USD exchange rate tanks versus EUR, GBP, RMG and JPY.

- Cheaper U.S. exports, more expensive imports lead to U.S. production growth.

- U.S. employers hire like crazy.

Appealing, right? In this case, the cost – inflation – is essentially exported to foreigners.

The problem, of course, is that it only works if every other major economy has the opposite problem – if their economies are too strong, their currencies too weak and their government debt loads well under control. Since that’s not the case, this kind of unilateral action would have catastrophic consequences because it would immediately trigger counter-devalutions from other countries. You’d get something like the devastating currency war triggered by the 1933 Smoot-Hawley Act.

It’s why, in this case especially, monetization must be jointly calibrated.

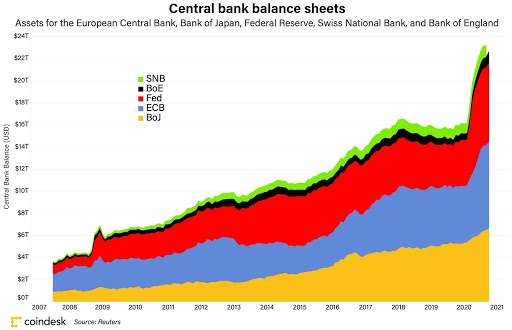

What does that look like? Well, for one, all central banks’ balance sheets would explode even more than they have already – see chart below. But this time it would likely be with bonds bought directly from their governments.

Governments would use the proceeds to repay creditors, the catch being that money, now in greater supply, would buy less than it had previously. The big question is whether this inflationary hit comes as a one-off price adjustment or breeds self-perpetuating hyperinflation – results would vary from country to country, depending on the degree of trust commanded by the government.

But whether they deliver a one-off transfer from creditors to savers or trigger an ongoing collapse that hurts everyone, those extra dollars, euros, yen and yuan must go somewhere. Because all currencies are increasing supply simultaneously, their holders will instead seek out scarce assets such as gold, real estate and, of course, bitcoin.

(Pro tip for the new president: While bitcoin (BTC) is well off its early January highs, its spectacular surge through December suggests people are seeing the scenarios play out. Its price is a useful temperature gauge. Keep your eye on it.)

New system

Setting aside the inflation challenge, there’s a structural problem with synchronized monetary policy: All currencies are not created equal, which makes it difficult to find common ground. The rules for the dollar, the one currency that’s universally used as a denominator for assets and liabilities outside of its home country, differ from others.

This creates incentive misalignments for the Federal Reserve, which has a mandate to serve the U.S. public but also acts a de facto lender of last report to the outside world.

We witnessed this last March. When the global economy seized up due to COVID-19, the world’s banks scrambled to find greenbacks to ensure they could meet their dollar obligations. So the Fed went on an asset-buying spree like never before, creating bank reserves and international swap lines that pumped trillions of dollars into the global banking system.

But what happens if the outside world’s interests conflict with those of the U.S.? What if the U.S. needs a weaker dollar but the world needs a stronger dollar?

Over time this mismatch has created imbalances in the global economy. Many economists worry that it’s approaching the breaking point.

Willem Middelkoop and David Marsh of the Official Monetary and Financial Institutions Forum, a high-level think tank, this week called on the U.S. and China to find a coordinated digital solution or face “monetary breakdown.” They point to former Bank of England Governor Mark Carney’s suggestion for a new, International Monetary Fund-coordinated digital international reserve currency as a possible mechanism. (Carney refers to this dollar-alternative as “synthetic hegemonic currency.”)

Is a multilateral currency the answer? Or might we instead just move to a common protocol enabling decentralized exchanges between central bank digital currencies and other digital assets such as bitcoin? In the latter case this new, programmable form of money could enable low cost exchange-rate hedging, making an intermediating reserve currency redundant.

The point is that although the U.S. seems all-powerful right now, digital alternatives to the dollar-centric financial system are emerging. Washington, Wall Street and Silicon Valley must be ready.

It’s a good sign you’re seeking to fill regulatory agencies with crypto-savvy leaders, all people well placed to address the big questions raised here. (See “Relevant Reads” below.)

But the changes coming will be huge. To navigate them will take leadership, a bold vision and an openness to new ideas.

Parabolic expansion

Consistent with the theme of this week’s column, a look at central bank balance sheets is in order.

This chart, produced by CryptoX’s Damanick Dantes and Shuai Hao, using the Federal Reserve Bank of St. Louis FRED database, gives a pretty good sense of the monetary expansion delivered by five of the world’s most important central banks over the past decade and a half, and especially in 2020.

They’ll likely do much, much more as a reckoning with debt and the COVID-19 fallout comes due. It’s why many bitcoin enthusiasts aren’t phased by this week’s pullback in its price.

The Conversation: CSW strikes again

“Faketoshi” is at it again.

Craig S. Wright, the man who wants you to believe he is Satoshi Nakamoto, is pulling more stunts. This time, he is doubling down on his May 2019 move to register a claim to Satoshi’s famous 2008 white paper with the U.S. Copyright Office, by sending takedown messages to two long-running Bitcoin sites: bitcoin.org and bitcoincore.org.

Upfront, let’s be clear: Anyone could have made the U.S. copyright registration. The registration is merely recognition that a claim has been made; it’s not proof of authorship. In fact, the U.S. Copyright Office took pains to clarify that after Wright’s registration, saying it “does not investigate the truth of any statement made” and that it “does not investigate whether there is a provable connection between the claimant and the pseudonymous author.”

Nonetheless, diverging responses from bitcoin.org and bitcoincore.org sparked yet another feisty debate over Wright’s actions and over how to deal with someone with a penchant for such legal actions.

Bitcoincore.org, which is associated with a group of developers focused on the upkeep of Bitcoin’s core protocol, decided to remove the white paper from its site. This prompted an angry reaction from Cobra, the pseudonymous moderator of bitcoin.org, who accused the moderators of bitcoincore.org of “surrendering” in a way that “has lent ammunition to Bitcoin’s enemies, engaged in self-censorship, and compromised its integrity.”

This, retorted long-time Bitcoin Core developer Greg Maxwell in a Reddit thread, is absurd. “With due respect, Cobra is just wrong about ‘capitulation’: The real capitulation is agreeing with the conman that his impotent drama about the white paper might matter or could really accomplish anything.”

Maxwell defended bitcoincore.org’s decision as a “pick your battles” move, arguing that it wasn’t worth letting the well-funded Wright force a costly legal battle when it does nothing to the resilience of Bitcoin itself. Taking it down didn’t matter, Maxwell said, because the MIT-licensed white paper is already everywhere. And “with publicity about this nonsense it’s going to get published in 1,000 more places.”

Sure enough, a race to host and re-publish the white paper quickly got underway. A Twitter thread by Jerry Brito, executive director of Coin Center, which started with a tweet listing five websites that were hosting the white paper and which asked, “Who else wants to join this party?”, just got longer and longer. By the end of the day, 124 replies were on that thread, most of which included fresh links to sites hosting the white paper. One reply, from Michael McSweeney at The Block, even pointed out that the U.S. federal government was one of the sites.

For the record, CryptoX has been hosting the white paper for some time. You can find it here. Free to read. Free to share.

Relevant reads: Biden’s crypto gang

Last week, we looked at the mostly positive responses in the crypto community to news that former Commodities Futures Trading Commission Chairman Gary Gensler was likely to become head of the Securities and Exchange Commission. The community likes people who understand the tech and there was good news to celebrate this week as well.

- We learned that former CFTC Commissioner Chris Brummer, who runs the DC Fintech Week out of Georgetown and has written a book on crypto assets, is expected to be nominated to lead that institution.

- The Wall Street Journal reported that former Treasury official Michael Barr is expected to be nominated to lead the Office of the Comptroller of the Currency, which regulates banks. As CryptoX’s Nikhilesh De pointed out, Barr was once a board member of crypto firm Ripple.

- And even after some tough words about bitcoin by Treasury Secretary and former Federal Reserve Chair Janet Yellen in her spoken Senate testimony Wednesday, bitcoiners were pleasantly surprised to find that her written testimony Thursday took a much more nuanced position toward the cryptocurrency.