The market for selling hash rate in exchange for Bitcoin (BTC) has undergone staggering growth in the epoch since the last halving. There is almost 100 times the level of competition today as there was four years ago, up 125 exahashes from 1.4 exahashes.

After the last halving in 2016, 16nm chips were first hitting the market, pushing 14 terahashes per second, or T/s, at an efficiency of 100 watts per terahash. Since then, 10nm, 7nm and now 5nm chips have switched on, with over 100 T/s now consuming just 30 W/T. Advancements in chip design and fabrication have more than doubled the efficiency of ASICs, and are nearly 100 times as powerful. While 5nm chips are only just beginning to join the network, the 7nm chip market has been expanding for a couple of years, forcing 16nm and 10nm chips to find cheaper electricity or capitulate. Mining operations have branched out internationally across energy markets, seeking cheaper electricity to widen profit margins and prolong the lifespan of their machines. Mining is a long game about survival.

There has been a great deal of discussion lately on how Bitcoin’s upcoming halving (less than two weeks away!) will affect the mining industry in the coming months. There is little doubt among researchers and industry experts that the hashrate is going to drop significantly when the block subsidy gets cut in half. Blockware Solutions recently released a report arguing that the halving will lighten sell pressure as older equipment and higher electricity costs squeeze out inefficient competitors.

The question is, how much hashrate will go offline? As pool operators, we don’t receive any information on miners’ electricity costs, so we can’t know exactly what that number will be, but by breaking down hashrate distribution, we can look at which miners have the highest risk of shutting down.

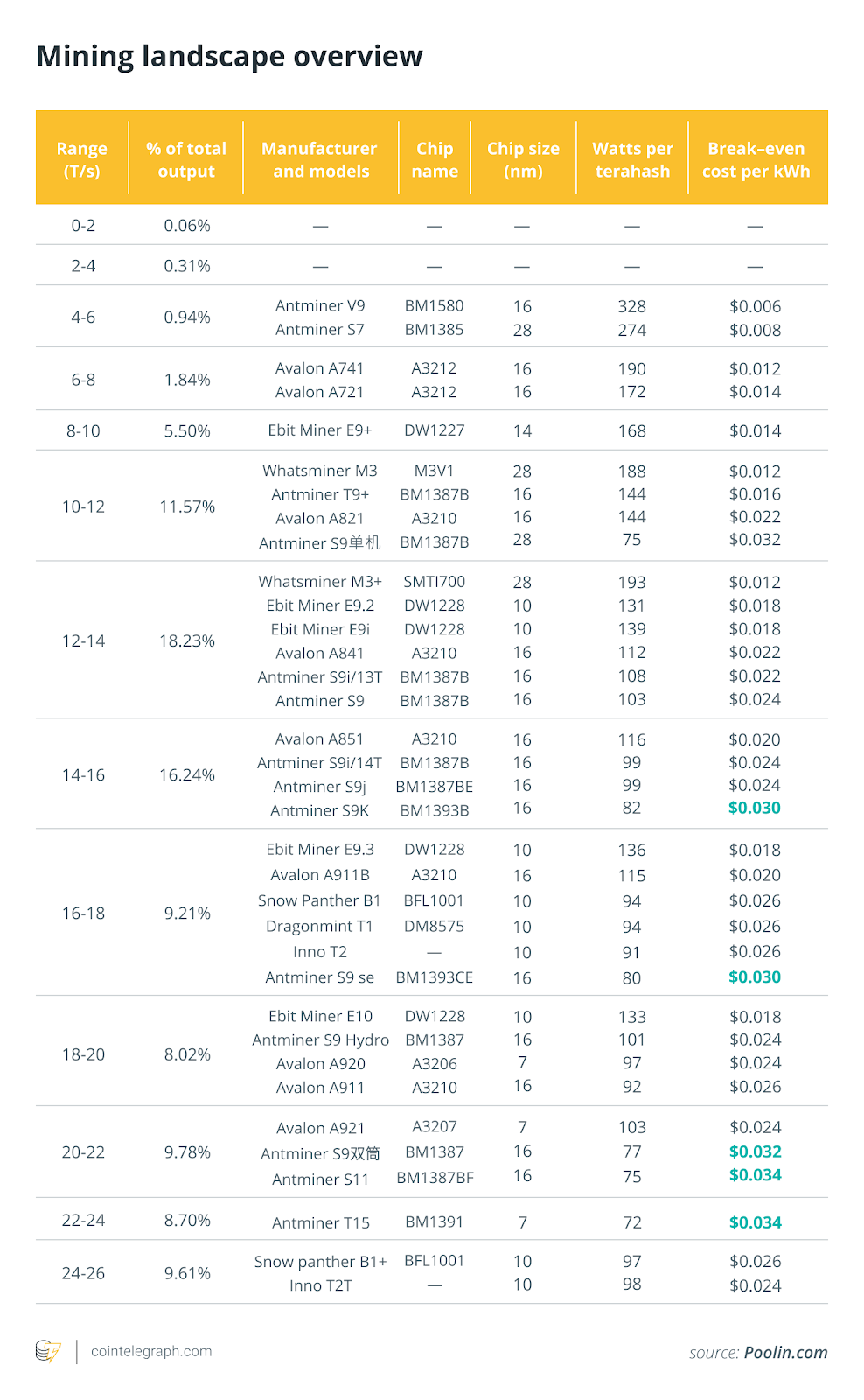

Below, you can see the lower quartile of total hashrate divided into two-terahash intervals. Each section of the pie chart represents the percentages of total output for each range in the lower quartile.

We’re looking particularly at the lower quartile of the network hashrate because this is the highest risk area, where miners’ profit margins are tightest. The range from 0–25 T/s represents the majority of the 16nm and 10nm chips, many of which are likely to capitulate once the block subsidy is halved. The most popular miner that was sold in the last four years was Bitmain’s S9, of which there are many versions, but they all fall between 12–22 T/s. The standard S9 produces 13.5 T/s, which probably accounts for the majority of miners in the 12–14 T/s range.

We estimate that the miners in this range account for approximately 15% to 30% of the Bitcoin network’s overall hashrate. While we expect that most of them will shut down after the halving, it is likely that some have cheap enough electricity to survive in the near future.

There are three changing variables that miners need to compare when calculating profitability: revenue, costs and difficulty. The price of Bitcoin and the block reward set the upper bound for income revenue. The halving of the block reward has the same effect on a miner’s revenue as halving the United States dollar price of Bitcoin. The recent price rally since hitting a yearly low means there could be room for wider profit margins in the short term if prices continue to rise. However, if the price were to drop, then inefficient miners will be squeezed out faster.

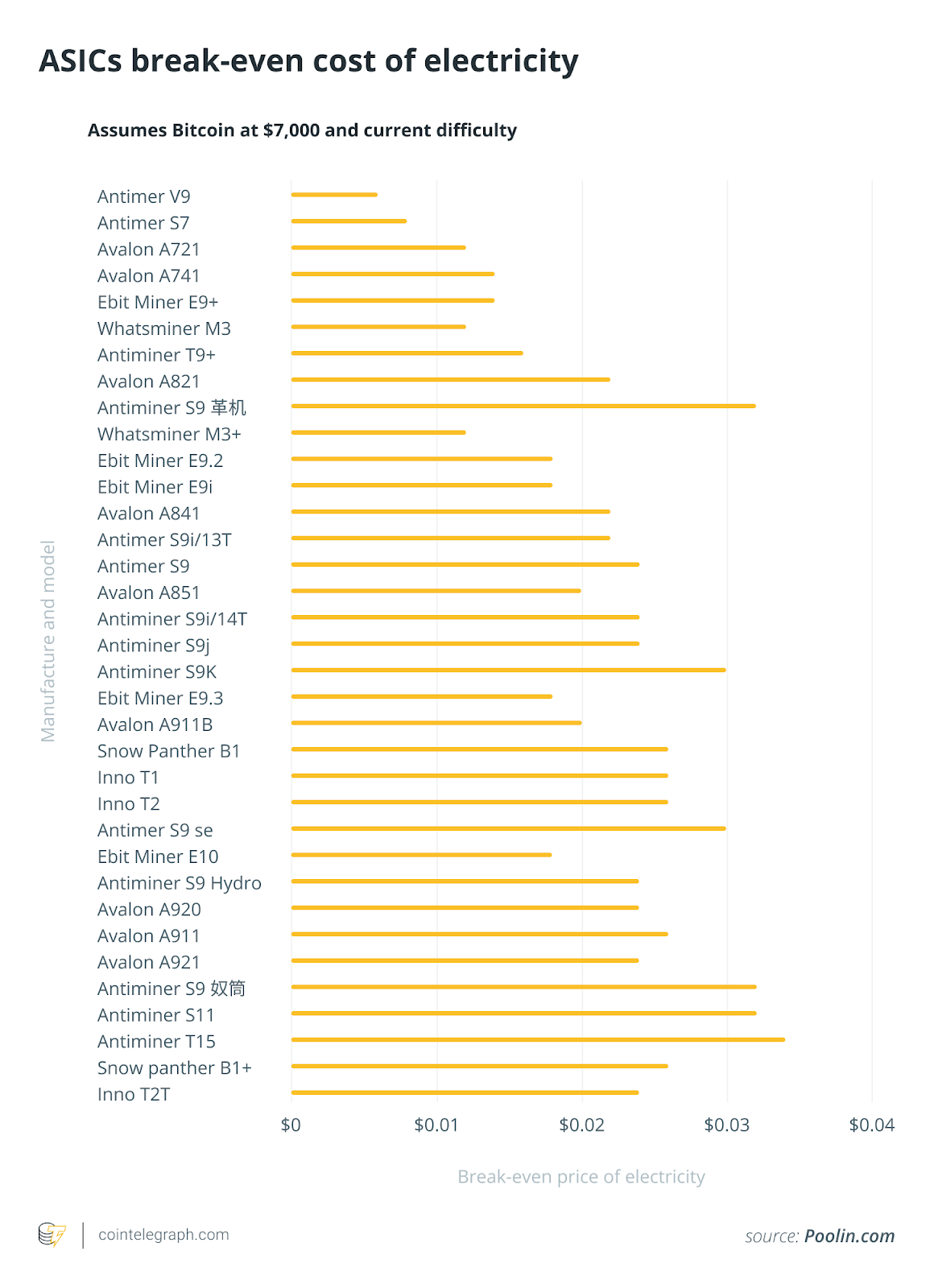

By comparing the break-even prices of miners across the lower quartile, we can see at what prices older miners will no longer be profitable. In order to compare break-even prices, we have to take the current difficulty and price into consideration. In the graph below, we suppose Bitcoin is at a price of $7,000 with the current difficulty.

The highest that any of these can pay for electricity and remain profitable after the halving is $0.034 per kWh. The lowest ranges operating at 0–10 T/s will all be leaving unless they have virtually free electricity and no other overhead costs. If we take the ranges with the largest percentages of hashrate, between 10–16 T/s, only the Antminer S9K barely breaks even at 3 cents per kWh. At 46%, this range represents nearly half of all hash-power mining in this range, most of which will need to mine below $0.02 per kWh to remain profitable after the halving. There are very few places that can offer such cheap electricity. Even the rates from hydroelectric dams in Szechuan, China during the rainy season are well above these breakeven costs. Even if some of these miners are able to survive with sub-$0.02 electricity, their margins will be so thin that if the difficulty continues to increase, they will eventually be phased out due to producing such miniscule profits. It is likely that most of the hashrate in this range will be lost from the outset.

Some of the miners from 16–26 T/s may be able to remain profitable a little longer after the difficulty adjusts downward, with more breakeven prices between $0.03 and $0.035 cents per kWh. However, these again will be razor-thin margins, which also makes these miners vulnerable to falling off in the short term. While there may be some that are able to remain working given cheap enough electricity, we estimate that less than 15% of the lower quartile will remain.

The upcoming and final difficulty adjustment with the 12.5 BTC block subsidy will occur one week before the halving (1008 blocks), and the difficulty is projected to increase. We expect that the first 1008 blocks after the halving will be mined slowly as huge numbers of unprofitable miners drop off the network. We estimate that closer to 30% will be squeezed considering that the first 1008 blocks will have the pre-halving difficulty, but half the reward.

After the first difficulty adjustment, some older miners may turn back on, but as new, more efficient ASICs come online in the coming months and existing miners find lower electricity prices, old generation miners will inevitably be phased out. Many of the older 7nm chips will take the place of cheap power, where 16nm and 10nm chips will have been just scraping by, while new 5nm chips will profit at higher electricity costs and apply more pressure downwards. There will undoubtedly be a series of fluctuations as new hashrate pushes out older equipment, stabilizes and then continues to move up.

The beginning of this mining epoch provides new miners an opportunity to enter a more stable environment, given that efficiencies in 5nm chips will likely remain profitable for the next four years or longer as we run up against the edge of Moore’s Law in how thin silicon wafers can go. New entrants can therefore have a clear picture of what the mining landscape will look like for the next four years.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cryptox.

Alejandro De La Torre is a staunch believer in the financial freedom that Bitcoin and cryptocurrencies will bring to humanity. He brings seven years of industry experience. Currently, De La Torre is the vice president of Poolin.com, a Bitcoin and cryptocurrency mining pool. Previously, he was the vice president of BTC.com and the business development manager at Blocktrail (acquired by Bitmain).