If, in the compressed time of blockchain existence, the “crypto winter” of 2018-2019 was Ethereum’s Dark Ages, then we’re now in its Renaissance.

But it’s an open question whether the blockchain platform and its enthusiastic community can take the wider world into the next era: the decentralized equivalent of the industrial revolution.

As Ethereum prepares to celebrate the five-year anniversary of its mainnet launch on July 31, billions of dollars in value rest on that question. Specifically, on whether the all-important Ethereum 2.0 scaling project can be successfully launched and integrated into its existing architecture.

By most measures, the Ethereum ecosystem is undergoing an impressive growth spurt. Record-breaking “gas” usage for smart contract and payment executions has now put Ethereum’s daily transaction fees totals above those of bitcoin. A strong rally in the price of ether (ETH) means Ethereum’s native token is among just a few leading cryptocurrencies, including bitcoin, Cardano’s ADA and Stellar’s XLM, to have more or less shaken off the sharp crypto selloff seen in March. And the amount of second-tier value locked into Ethereum smart contracts is ballooning, with total daily value transfers on Ethereum reaching that of Bitcoin in April.

You’re reading Money Reimagined, a weekly look at the technological, economic and social events and trends that are redefining our relationship with money and transforming the global financial system. You can subscribe to this and all of CryptoX’s newsletters here.

The growth is found in a variety of Ethereum-based applications.

Take decentralized finance, for starters. With the locked value in DeFi applications now above $1 billion, there’s an increasing array of products servicing this burgeoning ecosystem. This week, we learned of the successful launch of decentralized lender Compound’s new COMP token and that Nexus Mutual, a decentralized insurance provider to protect users against smart contract breaches, saw its pooled funds double to more than $4 million over the past 90 days.

There’s been similar growth in Ethereum-based stablecoins. This is dominated by dollar-pegged token Tether, which is widely used as a settlement and clearing mechanism by cryptocurrency exchanges and has seen spectacular issuance this year. As we reported in Money Reimagined two weeks ago, nascent demand for Ethereum-based stablecoins such as USDC is emerging in dollar-starved developing countries, where it’s being used for remittances and day-to-day payments.

Apart from these financial use cases, there are also healthy growth indicators in the software development economy that has arisen around Ethereum. For instance, the worldwide community of developers tapping into bug bounties and other projects funded through Gitcoin, an Ethereum-focused marketplace for open-source engineering work, has grown to almost 40,000.

According to analysis by Glassnode, the majority of ether transactions are now used to pay for a variety of smart contact commands rather than simple monetary exchanges between so-called externally owned accounts. That, along with a reduction in large-scale “whale” ether accounts, suggests transactions on Ethereum are now more connected to utility than to speculative activity.

The scaling imperative

These are encouraging signals. They reflect growing confidence the initial coin offering (ICO) bust is in the rearview mirror and that concerns about smart contract insecurity are diminishing.

But if the Ethereum community is to achieve its sweeping goal to create a decentralized economic system, it must function at scale. All hinges on Ethereum 2.0.

The two core components of the phased 2.0 transition are incredibly difficult to engineer for a decentralized system of this breadth: a foundational shift from a proof-of-work consensus algorithm to proof-of-stake blockchain, and an ambitious “sharding” effort to dramatically accelerate transaction processing.

These steps must happen in a phased way.

The development work first entails integrating a new proof-of-stake blockchain known as Beacon, and its related software clients into the legacy proof-of-work blockchain. With no corporate organizational structure to direct commands, all work is conducted by a giant, decentralized, hard-to-coordinate team, with armies of developers in far-flung parts of the globe earning bounties to detect bugs in the system’s sprawling codebase. That’s difficult.

And the importance of getting this right is underscored by Ethereum’s history. On numerous occasions malicious attackers have exploited smart contract loopholes and other security vulnerabilities to steal millions of dollars, most famously in 2016 with the $60 million DAO attack, more recently in the $25 million loss at DeFi protocol dForce.

For all those reasons, Ethereum developers can be excused for the long delays in rolling out 2.0. But they’ll eventually need to flip the switch and start the initial Beacon implementation because, at some point, delays themselves can eat into confidence among participants.

For now, Ethereum 2.0 appears to be enjoying an optimism lift.

Codefi, a financial services platform based at influential Ethereum development lab ConsenSys, this week announced it would pilot a new staking-as-a-service ether product backed by cryptocurrency heavyweights Binance, Huobi Wallet, Matrixport, Crypto.com, DARMA Capital and Trustology. Such services act on behalf of holders of proof-of-stake cryptocurrencies to stake them for block rewards. In effect, it turns cryptocurrency custodial holdings into quasi interest-bearing accounts. Needless to say, the service will only work if and when Ethereum transitions to proof-of-stake.

During CryptoX’s Consensus Distributed conference last month, Ethereum founder Vitalik Buterin retracted an earlier comment that Ethereum 2.0 was likely to launch in July. However, he did indicate all the pieces are falling into place for a more scalable, private system to come online soon.

A tiny pond fight

Despite all this progress, the Ethereum economy is still just a tiny dot within the $88 trillion global economy. If it is to change the world, scalability and adoption need to happen.

And because the opportunity is so large compared to its current footprint, there’s no guarantee Ethereum becomes the standard, despite its early lead on other blockchains.

Charles Hoskinson, founder of competing blockchain Cardano, told Ryan Selkis of Messari on Thursday that Ethereum’s claim to have gained unbeatable “network effects” is the “biggest lie ever told in this space.” Ethereum calling itself “the dominant platform” is “like saying you’re the biggest fish in a tiny pond right next to the ocean,” he said.

Hoskinson argues Cardano’s moves in developing countries will let it seize the pole position in a part of the world likely to leapfrog the industrialized world with decentralized technology. But to suggest Ethereum doesn’t have a head start and an advantage is naive. The breadth of developer and transaction activity generates real-world value in a self-fulfilling expansion, as it unlocks funds for Ethereum protocol and dapp developers to do yet more work on new solutions and to bring even more participants into the ecosystem.

Even if it doesn’t win, no one, not even the most hardened bitcoin maximalist, can deny the Ethereum community has fostered some powerful, outside-the-box, innovative ideas for a future economy. It’s these kinds of ideas that will shape the Web 3.0 world to come.

Bitcoin, tech stock

Last week, we, among other outlets, remarked on bitcoin’s closer correlation with U.S. stocks. Both the rally to a four-month high near $10,000 and the subsequent drop last week coincided with similar movements in broad indexes such as the S&P 500. It raised the question: Is bitcoin now solely to be lumped into a broad category of “risk assets?”

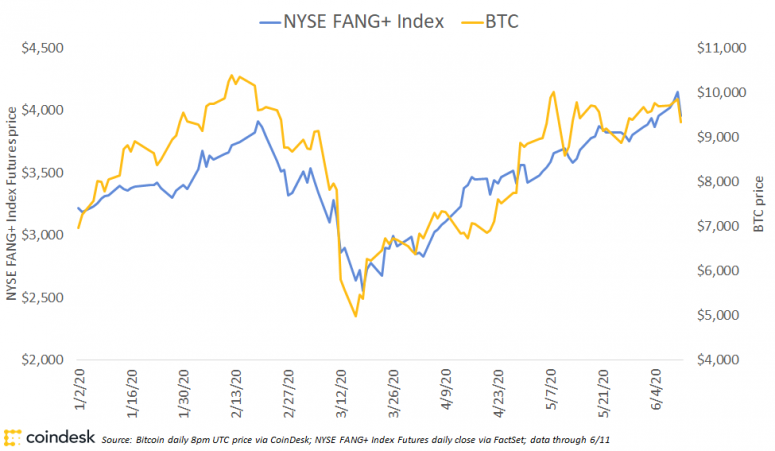

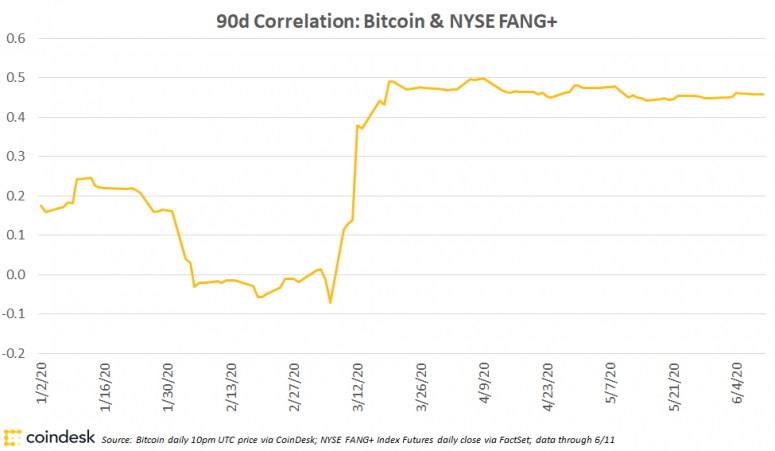

But here’s another, more pointed question: Why is bitcoin behaving like an internet network platform? Charlie Morris of ByteTree noted a remarkable correlation between the price of BTC and the NYSE’s FANG+ index. That index’s eight component stocks include six internet juggernauts – Facebook, Apple, Amazon, Netflix, Alphabet (Google), Twitter, Alibaba and Baidu – alongside electric carmaker Tesla and GPU provider Nvidia. Its performance is very much tied to the social network connectivity and data aggregation benefits that the internet has delivered to those dominant platforms. Here’s a chart of bitcoin’s performance against that index.

The relationship has not always been there. As this chart shows, the NYSE FANG+ index and bitcoin were showing essentially zero correlation before March.

What is this telling us? Well, first, remember the golden rule: Correlation is not causation. But it’s nonetheless tempting to speculate that in the COVID-19 work-from-home era, cryptocurrencies are being viewed as part of a suite of technologies enabling a decentralized, online economy.

The Global Town Hall

NOT JUST CRYPTO. If it’s frustrating for crypto traders to find that bitcoin and other cryptocurrencies can’t perform on their own terms at the moment, maybe they’ll take some comfort from the fact they are not alone. Foreign exchange traders are also finding currencies behaving as if their value is dependent on stocks. As Eva Szalay at the Financial Times reports, currencies such as the Australian dollar and the British pound, whose fate is normally directly determined by macroeconomic conditions, are now caught in the same “risk-on/risk-off” trading whims of the stock market. It’s yet another way in which the Federal Reserve’s massive monetary stimulus efforts during the COVID-19 crisis are distorting the functioning of our financial system. Like a broken record, let’s say it again: To protect the fabric of our economies and societies, we need a new system for spurring economic activity, one that doesn’t skew it toward the interests of hedge funds and instead encourages innovation and gets resources to those who most need it. Wall Street-centric solutions aren’t working.

DON’T LISTEN TO TINA. The history of financial crises shows the most dangerous assumption in investing is that a particular bet is a sure thing. (Think of the flawed pre-2008 notion that housing prices always go up.) The same goes for the assumption the U.S. dollar will always be propped up by the demand of foreign governments, companies and financial institutions, which need it as a reserve asset or as a trade-intermediating instrument.

Economist Stephen Roach, formerly chairman of Morgan Stanley Asia and now a professor at Yale, is taking it upon himself to warn against that assumption. He’s predicting a 35% plunge in the value of the dollar against its trading partners’ currencies, telling CNBC it will “fall very, very sharply.” A move like that would have far-reaching fallout in a global economy where assets and liabilities are heavily dollarized, which is one reason critics of dollar bears like Roach say it won’t happen: because there’s too much at stake. In a supporting column for Bloomberg, Roach called this pro-dollar argument the TINA case – for “there is no alternative” – and he warned of its complacency. With the U.S. now acting against globalization and running dangerously high debt levels, the reasons for foreigners to lose faith in the dollar are rising, he wrote. No mention of the role that cryptocurrencies or stablecoins might play in this, but it’s a reminder the existing framework for the dollar-dominated global economy is ripe for newly imagined form of money.

TRANSPARENCY PLAY. Latin America is proving to be a fairly receptive place for blockchain and cryptocurrency solutions — including among governments. A big part of that stems from the proactive work of the Inter-American Development Bank, which has launched a variety of pilots and experiments in the region. In April, CryptoX’s Leigh Cuen reported on a project led by an IDB-sponsored project led by startup Emerge to improve health record keeping amid the COVID-19 crisis. Now, it’s partnering with the World Economic Forum to work with the Colombian government on a blockchain project aimed at adding transparency to official procurement and curtailing corruption. Just a proof-of-concept at this stage, but at a time when other developing nations are facing a crisis of trust in their governments, which undermines faith in their currencies, innovative efforts to boost trust could pay dividends.

Relevant Reads

‘Snake Oil and Overpriced Junk’: Why Blockchain Doesn’t Fix Online Voting. Fears about an election failure in November are widespread. But as Benjamin Powers reports, internet security experts are warning governments to stay away from blockchain-based online voting systems.

Delta Exchange Launches Crypto Interest Rate Swaps. Lending rates in crypto can swing wildly, which makes investing in them tricky and not conducive to encouraging credit. Enter a hedging solution: decentralized interest rate swaps. Omkar Godbole reports.

The New York Times Proves Why Civil’s Vision Is Still Vital. Civil, the token-based system for creating less-hierarchical, decentralized newsrooms, flamed out recently amid a host of problems. But as columnist Cathy Barrera points out, the principles of that concept would prove valuable in the current moment of tension and disinformation around Black Lives Matter.

US Fed Chair Says Private Entities Should Not Help Design Central Bank Digital Currencies. In a mark of how much digital currencies are now seizing mindshare among central banks, Federal Reserve Chairman Jerome Powell weighed in on CBDCs again during congressional testimony. This was to warn against “privatizing the money supply.” Nikhilesh De reports.

Thailand to Raise $6.4M With Sale of Blockchain-Based Bonds. A Thai government blockchain-based sale of saving bonds was based on tokens as small as one baht ($0.032). Fragmented ownership opens up opportunities for the poor to invest. Jaspreet Kalra reports.

When Ferrari? Tokenized Supercar Gives European Investors Exposure to Asset Class. Similar concept, very different market. Tokenization allows for fragmented ownership of luxury cars worth $1.1 million. By Paddy Baker.

In the Wildcat Era of Stablecoins, Commercial Banks Have New Rails to Ride. Is the booming stablecoin market destined for the same regulatory constraints that eventually came to wildcat banking in the 1800s? The parallels between the two eras, as columnists Chance Barnett and Michael Dowling point out, are quite striking.

The leader in blockchain news, CryptoX is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CryptoX is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.