Max Boonen is the founder and CEO of crypto trading firm B2C2. This post is the third in a series of three that looks at the structure of crypto markets. Opinions expressed within are his own and do not reflect those of CoinDesk.

In the two previous articles, I summarized the evolution of speed in modern finance and the balancing act between good and bad latency reductions. Let us now examine the venues where trading takes place and how they fare in this world of increasing speeds.

To trade financial assets, a variety of market designs are possible: those are called market microstructures. We will explain three major ones found in crypto today, why they exist and how one should evaluate them.

This is the classic exchange, represented in popular culture by the ubiquitous facade of the NYSE. What exchanges provide is known as a central limit order book (“CLOB”). It is central because all participants send orders to it. It is “limit” because the price specified by an order indicates the limit (worst) price at which the trader is willing to transact. Any new order either trades against a pre-existing, opposite order or remains in the order book at its limit price. Participants can therefore both execute instantly against resting orders (to “take,” to be “aggressive”) or wait for execution by others (to “make,” to be “passive”). By and large, those passive orders are placed by professional market makers. Importantly, trading in a CLOB is entirely anonymous – or so one hopes – pre-trade and normally post-trade, too: the exchange sits in the middle of all trades. Traders pay commissions, often with volume discounts.

The single-dealer platform

On a single-dealer platform, or SDP, clients trade with one liquidity provider (conventionally, either a bank or a so-called non-bank liquidity provider such as B2C2) on a “name disclosed” basis, since the dealer runs the proprietary platform and knows who is trading. Clients “take” and the dealer “makes” as a principal, meaning that when a client buys, the dealer sells and vice versa. This is not to be confused with an agency model where the middleman transmits client orders to an actual dealer or venue. In the dealer model, there is no commission but the client faces a variable bid-offer spread to compensate the market maker for the financial risk it is taking. B2C2’s over-the-counter (OTC) platform was the first single-dealer platform in crypto, having operated since 2016. Unlike an exchange, not all participants see the same price; in fact, there may be as many unique price feeds as counterparties, for reasons that go way beyond simply rewarding big customers with favorable terms.

Instead of receiving one single feed, clients receive an aggregation of different prices and can pick the best one. While diverse in their mechanics, aggregators put market makers on one side and price takers on the other. A crypto example is CoinRoutes. Takers are normally anonymous before the trade with disclosure of the counterparty to the liquidity provider after the trade. Aggregators are not exchanges! First, the settlement relationship is often (but not always) bilateral, meaning the takers must be onboarded by each liquidity provider they want to interact with, and bilateral credit limits have to be respected. Second, and crucially, the makers typically cannot take. Aggregators, like exchanges, charge a commission.

Adverse selection: a tension within all markets

Where should one trade? The answer depends on the interaction between your trades and the liquidity provider(s) on the other side.

Imagine you want to bet on the winner of the 2020 U.S. presidential election. You’ve done your research and feel quite confident. One person in particular is keen to take the other side of your bet: the famous statistician Nate Silver. Do you still want to bet?

While an election represents the sum of each person’s vote, few can predict its outcome; the same goes in financial markets. Most participants do not know where the market is going; those who do are called informed traders. When it comes to the U.S. political landscape, Nate Silver is informed because he might know something you don’t and his willingness to bet against you is an indication of that. This is adverse selection.

Note that being informed nowadays means being fast. It does not actually refer to knowing where the price will be a month, a day or even an hour from now. As renowned economist Andrew Haldane put it:

“Adverse selection risk today has taken on a different shape. In a high-speed, co-located world, being informed means seeing and acting on market prices sooner than competitors. Today, it pays to be faster than the average bear, not smarter. To be uninformed is to be slow.”

Recall my previous post on the latency arms race. In the high-frequency context where market-making takes place, the most brilliant quantitative fund might be considered uninformed as long as it is not operating in the high-frequency spectrum. Market makers have to balance the losses incurred against informed traders with the spread they earn from everyone else.

Diff’rent strokes: What might be right for you might not be right for some

Exchanges are the venues with the highest adverse selection because everyone can take indiscriminately and anonymously. Aggregators come in second since they are partly anonymous but the makers cannot take. As explained in Part 1, market makers are also high-speed informed traders, thus a venue lowers its average toxicity by preventing the makers from taking. Lastly, bilateral relationships have the least adverse selection since the dealer knows exactly how informed any individual client is. In essence, the spectrum represents a trade-off for the investor between receiving better prices at the cost of disclosing more information or being turned down altogether.

As a result of the tension above, markets naturally iterate through the following cycle:

1) informed traders are identified by liquidity providers as less profitable trading relationships

2) liquidity providers thus show more conservative prices to more informed traders, and more competitive pricing to everyone else

3) the most informed traders have no choice but to switch to more anonymous venues: aggregators first, then exchanges

4) adverse selection becomes exacerbated on exchange due to the arrival of those new informed traders, thus the market impact (broadly defined) of trading increases, incentivizing uninformed traders to leave exchanges in favor of direct relationships with market makers where they receive comparatively better pricing

5) rinse and repeat until such time as there is strong self-selection of traders: on one side, high-speed, informed trading with high market impact on exchanges; on the other, less expensive liquidity in the OTC market.

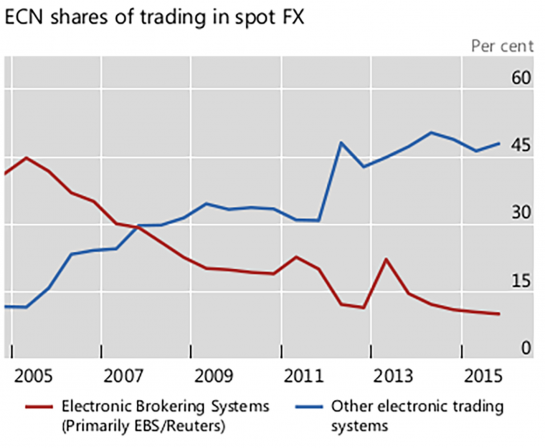

This is what has happened in the foreign exchange market over the past 10 years. EBS and Reuters, the primary CLOBs, lost market share to single-dealer platforms as the arrival of high-frequency trading firms in the FX market pushed banks to retrench in favor of direct OTC relationships.

Per the BIS, “On the one hand, liquidity provision has become more concentrated among the largest banks, which reap the benefits of a large electronic network of client relationships to internalize a large part of their customer flows. Many other banks, however, have found it hard to compete and have resorted to an agency model of market-making or have exited the business altogether.”

The same evolution marked crypto in 2019. Exchange market-making has become extremely competitive after the entry of big high-frequency trading firms in early 2018 while the technological cost of running a single-dealer platform – as opposed to the voice trading of yore – forced crypto trading firms to adapt. We now witness a separation between a handful of principal dealers like B2C2, and firms focused on OTC redistribution (the agency model).

A separate dynamic is at work with aggregation, one that has yet to play out in crypto.

At first glance, it is always better to have more liquidity providers than fewer. But that’s wrong, because it takes two to tango. A measure of it is good, but too much and adverse selection again rears its ugly head.

The reason: winner’s curse. In an exclusive relationship, the liquidity provider executes all the client’s trades, good and bad. With a dozen aggregated liquidity providers, having shown the best price often means that it was too good a price, irrespective of how informed the client actually is. As a consequence, liquidity providers worsen pricing parameters for highly (and naively) aggregated flow. Research by Deutsche Bank explains how aggregation can worsen execution for uninformed (!) traders, with higher rejections and wider spreads.

Crypto might not go through a round of higher-than-warranted aggregation before the pendulum swings back as it did in the FX market. First, there are few electronic liquidity providers in crypto and fewer still that are good enough to deal with aggregation. Second, maintaining numerous separate relationships is operationally costly, especially with exchanges in an industry where the mantra is “not your keys, not your coins.” To paraphrase Matt Levine, no need to painfully re-learn the lessons of venue selection in conventional markets!

Conclusion: The right tools for the right task

I predict 2020 will be a year where, unsatisfied with exchange pricing (in terms of fees and market impact), large traders rethink their relationships with exchanges. In doing so, looking at fees and spreads is not sufficient. Assessing how one’s activity pushes the market against oneself must be part of the toolbox, too, and more. You don’t know how to swim just because you bought inflatable armbands.

A healthy, sustainable trading relationship is one that is profitable for both sides. The smartest price takers will not adopt a one-size-fits-all policy. They will route orders to the most appropriate venue based on the characteristics of the underlying flow or strategy. Latency-sensitive strategies should be executed on an exchange. Everything else should be sent to an aggregator or to a single-dealer platform.

The platforms face the flip side of this challenge:

● Exchanges must accept that the all-to-all model creates winners and losers; it’s a delicate balance to ensure the losers don’t move elsewhere.

● Aggregators must perform some degree of client selection to manage their toxicity profile (the famous lawsuit against Barclays’ dark pool is informative).

● Dealers must understand their clients’ business model and execution strategy to provide the right price to the right counterparty. We at B2C2 excel at this.

This might sound overly complex or premature but the days of easy money are gone. A dramatic compression in OTC spreads has been reported elsewhere and other segments are next. Derivative exchanges have started undercutting one another on fees. Custody fees have been slashed and will shrink again. I have seen many prospective funds or ETF sponsors project that they will be able to charge over 2 percent of assets under management. Forget about it.

When the overall cost structure of our industry goes down by half, the companies that do not want to worry about one or two basis points on the execution front will go bust. What will you do?

Disclosure Read More

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.