Bitcoin’s price surge may be driven as much by a drying up in supply as by an increase in demand.

That’s because Chinese miners are struggling to sell their crypto in ways that would quickly get them much-needed cash in the face of a government crackdown on local exchanges.

“The lack of supply has fed extremely well to the trendiness of this rally, without any of the large sell-downs typical of miner activity in the past,” Singapore-based trading firm QCP Capital noted in its Telegram channel.

QCP’s interpretation of the rally is simpler and less exciting than some of the other popular explanations, which cite macro factors such as demand for a hedge against monetary and fiscal indiscipline, an impending rise in inflation across the developed world, and search for yield as primary reasons for the price surge.

Miners mostly operate using cash and offload their bitcoin holdings onto the market almost daily to fund their expenses, mainly electricity costs, which are to be paid in the local currency (yuan, in the case of those operating in China). That makes miners constant sellers, and their actions influence the market price.

However, Chinese miners, who control over 70% of bitcoin’s hashrate or mining power, have been facing challenges liquidating their crypto holdings for cash because many are finding their bank accounts and cards frozen as a part of the Chinese government’s nationwide crackdown on telecommunications fraud and money laundering via cryptocurrency deals.

Currently, 74% of the miners are facing difficulty liquidating their holdings to meet electricity expenses, a Chinese crypto watcher going by the name Wu Blockchain mentioned on his Weixin blog, according to QCP Capital. Thomas Heller, formerly global business director at the mining pool F2Pool and now chief operation officer of mining and media firm HASHR8, confirmed the Chinese miners’ predicament earlier this week, saying it’s currently a “challenge” for Chinese miners to convert bitcoin and tether into cash.

The industry has been suffering ever since the Chinese authorities began freezing bank accounts in June and the situation has worsened in the past couple of months.

“Mining pools were selling large chunks of bitcoin in early September through exchanges, but this was hastily halted as their last remaining fiat off-ramp avenues were impacted with the arrest of large exchange heads like Star Xu and other [over-the-counter] brokers,” QCP Capital said.

Miner selling pushed bitcoin lower, roughly from $12,000 to $10,000, according to QCP Capital. The supply, however, dried up after the cryptocurrency exchange OKEx’s accounts were frozen in October.

That, coupled with increased institutional participation or large buying in the spot market, created a supply crunch, allowing an exaggerated bullish move.

Bitcoin is currently trading at $17,700, representing an over 140% year-to-date gain. Prices are short $2,500 of the record high of nearly $20,000 reached in December 2017.

Rally overstretched?

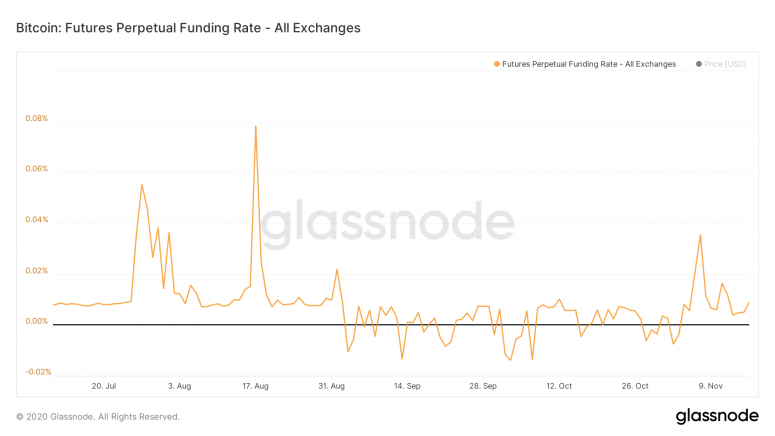

Sharp price gains are often accompanied by a big jump in the funding rate, the mechanism used by exchanges offering perpetuals (futures with no expiry) to balance the market and guide the perpetuals price toward the spot price.

The funding rate is positive, or longs pay shorts, when the perpetuals trade at a premium to the spot price, indicating stronger buying pressure. Alternatively, when perpetuals trade at a discount to the spot market, the funding rate is negative and shorts pay funding to longs.

A very high funding rate is widely considered a sign of an overextended bull run and often paves the way for a price pullback. For instance, the funding rate surged from 0.008% to 0.078% in the first half of August as bitcoin rallied to multi-month highs above $12,450. The cryptocurrency deflated to $9,800 by the second week of September.

This time, the funding rate has remained steady below 0.010%, meaning the cost of holding long positions is still considerably lower than in mid-August. Hence, a meaningful correction could continue to remain elusive, allowing further upside in the near term, possibly above record highs.

As per QCP Capital, the spot market imbalance driving the price has allowed the leverage funding market to remain stable throughout the recent bullish move.