Tensions between the Bitcoin and Ethereum tribes have been stirred by a trend that outsiders might see as a sign of harmony.

Throughout June, the amount of tokenized bitcoin on Ethereum, the bulk of it in WBTC, a special ERC2 token known as “wrapped bitcoin,” soared from 5,200 BTC to 11,682 BTC – now worth around $108 million – according to btconethereum.com.

As is their wont, each faction described the growth of WBTC tokens, whose value is pegged one-to-one against a locked-up reserve of actual bitcoin, as proof of their coin’s superiority over the other. The Ethereum crowd said it showed that even BTC “hodlers” believe Ethereum-based applications provide a better off-chain transaction experience than platforms built on Bitcoin, such as Lightning or Blockstream’s Liquid. Bitcoiners, by contrast, took it as confirmation that people place greater value in the oldest, most valuable crypto asset, than in Ethereum’s ether token.

You’re reading Money Reimagined, a weekly look at the technological, economic and social events and trends that are redefining our relationship with money and transforming the global financial system. You can subscribe to this and all of CryptoX’s newsletters here.

Beneath the rivalry on Crypto Twitter, the bitcoin-on-Ethereum trend says more about complementarity than competition.

The data simultaneously highlight that bitcoin is the crypto universe’s reserve asset and that Ethereum’s burgeoning “DeFi” ecosystem is crypto’s go-to platform for generating credit and facilitating fluid exchange.

Real world parallels

Though it’s too early to know who the eventual winners will be, I believe this trend captures the early beginnings of a new, decentralized global financial system. So, to describe it, an analogy for the existing one is useful: bitcoin is the dollar, and Ethereum is SWIFT, the international network that coordinates cross-border payments among banks. (Since Ethereum is trying to do much more than payments, we could also cite a number of other organizations in this analogy, such as the International Swaps and Derivatives Association (ISDA) or the Depository Trust and Clearing Corporation (DTCC).)

So, let’s dismiss claims like those of Ethhub.io co-founder Anthony Sassano. He argued that because bitcoin token transactions on Ethereum deny miners fees they would otherwise receive on the bitcoin chain, bitcoin is becoming a “second-class citizen” to ether. You’d hardly expect people in countries where dollars are preferred to the local currency to think of the former as second class. And just as the U.S. benefits from overseas demand for dollars – via seignorage or interest-free loans – bitcoin holders benefit from its sought-after liquidity and collateral value in the Ethereum ecosystem, where it lets them extract premium interest.

Still, to declare bitcoin the winner based on its appeal as a reserve asset is to compare apples to oranges. Ether is increasingly viewed not as a payment or store-of-value currency but for what it was intended: as a commodity that fuels the decentralized computing network orchestrating its smart contracts.

That network now sustains its financial system, a decentralized microcosm of the massive traditional one. It takes tokenized versions of the underlying currencies that users most value (whether bitcoin or fiat) and provides disintermediated mechanisms for lending or borrowing them or for creating decentralized derivative or insurance contracts. What’s emerging, albeit in a form too volatile for traditional institutions, is a multifaceted, market for managing and trading in risk.

This system is being fueled by a global innovation and development pool bigger than Bitcoin’s. As of June last year, there were 1,243 full-time developers working on Ethereum compared with 319 working on Bitcoin Core, according to a report by Electric Capital. While that work is spread across multiple projects, the size of its community gives Ethereum the advantage of network effects.

Whether DeFi can shed its Wild West feel and mature sufficiently for mainstream adoption, the code and ideas generated by these engineers are laying the foundation for whatever regulated or unregulated blockchain-based finance models emerge in the future.

Complexity vs simplicity

There are legitimate concerns about security on Ethereum. With such a complex system, and so many different programs running on it, the attack surface is large. And given the challenges the community faces in migrating to Ethereum 2.0, including a new proof-of-stake consensus mechanism and a sharding solution for scaling transactions, it’s still not assured it will ever be ready for prime time.

Indeed, the relative lack of complexity is one reason why many feel more comfortable with Bitcoin Core’s security. Bitcoin is a one-trick pony, but it does that trick – keeping track of unspent transaction outputs, or UTXOs – very well and very securely. Its proven security is a key reason why bitcoin is crypto’s reserve asset.

Base-layer security is also why some developers are building “Layer 2” smart contract protocols on Bitcoin. It’s harder to build on than Ethereum, but solutions are evolving – one from Rootstock, for example, and more recently, from RGB.

And while Ethereum fans crow about there being 12 times more wrapped bitcoin on their platform than the mere $9 million locked in the Lightning Network’s payment channels, the latter is making inroads in developing nations as a payment network for small, low-cost bitcoin transactions. Unlike WBTC, which requires a professional custodian to hold the original locked bitcoin, Lightning users need not rely on a third party to open up a channel. It’s arguably more decentralized.

Toward anti-fragility

At the same time, the inclusion of bitcoin in Ethereum smart contracts is inherently strengthening the DeFi system.

Decentralized exchanges (DEXs), which allow peer-to-peer crypto trading without centralized exchange (CEX) taking custody of your assets, have integrated WBTC into their markets to boost the liquidity needed to make them viable. Sure enough, DEX trading volumes leapt 70% to record highs in June. (It helped, too, that June saw a surge in “yield farming” operations, a complicated new DeFi speculative activity that’s easier to do if you maintain control of your assets while trading.)

Meanwhile, the recent move by leading DeFi platform MakerDAO to include WBTC in its accepted collateral has meant it has a bigger pool of value to generate loans against.

This expansion in DeFi’s user base and market offerings is in itself a boost to security. That’s not just because more developers means more code vulnerabilities are discovered and fixed. It’s because the combinations of investors’ short and long positions, and of insurance and derivative products, will ultimately get closer to Nassim Taleb’s ideal of an “antifragile” system.

That’s not to say there aren’t risks in DeFi. Many are worried that the frenzy around speculative activities such as “yield farming” and interconnected leverage could set off a systemic crisis. If that happens, maybe Bitcoin can offer an alternative, more stable architecture for it. Either way, ideas to improve DeFi are coming all the time – whether for better system-wide data or for a more trustworthy legal framework. Out of this hurly burly, something transformative will emerge. Whether it’s dominated by Ethereum or spread across different blockchains, the end result will show more cross-protocol synergy than the chains’ warring communities would suggest.

Gold “To The Moon”

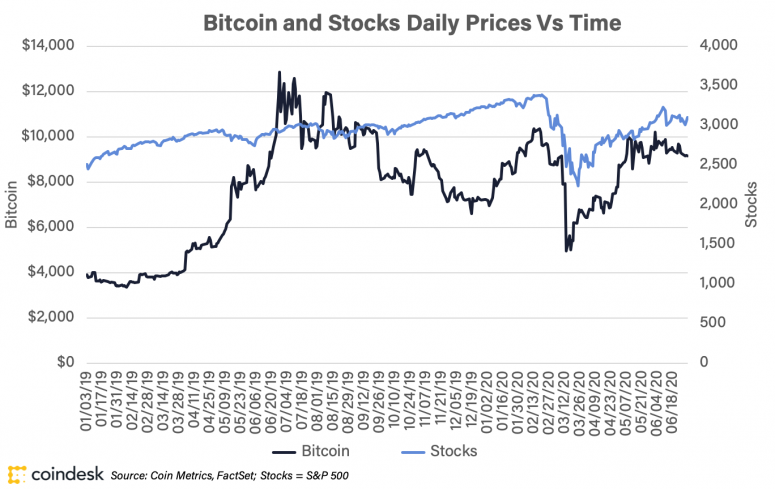

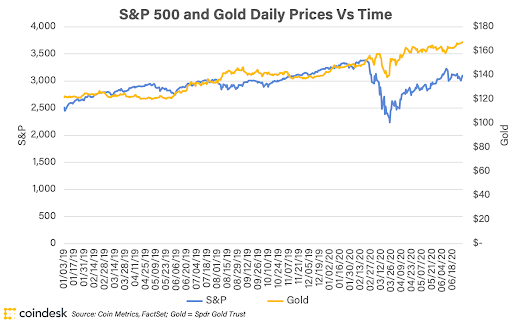

Bitcoin might be a reserve asset for the crypto community but its recent price trajectory, with gains and losses tracking equities, suggest the non-crypto “normies” don’t (yet) see it that way. Given the COVID-19 crisis’s extreme test of the global financial system and central banks’ massive “quantitative easing” response to it, that price performance poses a challenge to those of us who see bitcoin’s core use case as an internet era hedge against centralized monetary instability. Far from complying with that “digital gold” narrative, bitcoin has performed like any other “risk-off” asset. Meanwhile, actual gold has shaken off its own early-crisis stock market correlation to chart an upward course. While bitcoin has repeatedly failed to sustainably break through $10,000, bullion has rallied sharply to close in on $1,800, levels it hasn’t seen since September 2012. Some analysts are predicting it will breach its all-time intraday high of $1,917, hit in the aftermath of the last global financial crisis in 2011. To add insult to injury, one Forbes contributor even stole from the crypto lexicon to describe the state of play, telling his readers that gold prices are “soaring to the moon.”

Two charts below show the divergent fortunes of these two would-be safe havens. Throughout 2019, bitcoin seems far less correlated with the S&P 500 stock index than gold is. Come the collapse in March 2020, they seem to swap circumstances.

How to reconcile this? Time.

Gold has had at least three millennia to establish itself as a store of value people turn to when social systems are in stress. Bitcoin has only existed for 11 years and while plenty of investors are willing to speculate on the possibility that it might supplant or compete with gold, the idea is far from ingrained across society. When will it be more widely accepted? Perhaps when the international crisis of global leadership unleashed by COVID-19 undermines the capacity of institutions like the Federal Reserve to sustain economic and social confidence. Whatever new institutions and systems we create going forward will need to address how the internet has upended society’s centralized systems of governance. When that happens, we’ll need a decentralized, digital reserve asset as the base value layer. As I said, it will take time. Meanwhile, the developers will keep building.

Global Town Hall

TRUST ME, BOND MARKET, PLEASE. James Glynn at The Wall Street Journal had a piece this week about how the Federal Reserve is considering following Australia’s lead in using “yield caps” as a policy tool to keep long-dated interest rates down. The thinking is that if the central bank explicitly signals it will always institute bond-buying if the yield on a benchmark asset such as the 10-year Treasury note rises above some predefined ceiling, the market will be less inclined to prematurely believe the Fed is going to start tightening monetary policy. In other words, we won’t see a rerun of the 2013 “Taper Tantrum,” when the U.S. bond market, worrying that the Fed would start tapering off its bond-buying, or quantitative easing, drove down bond prices, which pushed up yields. (For bond market newbies, yields, which measure the effective annual return bondholders will earn off a bond’s fixed interest rate when adjusted for its price, move inversely to price.)

The yield cap policy would be new for the Fed, but it’s really an extension of an ongoing effort to do one thing: get the market to believe its intentions. The way monetary policy works these days, it’s meaningless unless the market behaves according to what the Fed wants. It’s not about what the central bank does per se; it’s about what it says and whether those words are incorporated into investor behavior. But the more it doubles down on this, the more the Fed creates situations in which it risks having its words held against it. And that puts it at risk of losing its most important currency: the public’s trust. Commitments to price targets are always especially risky – ask Norman Lamont, the UK Chancellor of the Exchequer, who had to abandon the pound’s currency peg in 1993 because the market didn’t believe the U.K. would back its promises. The Fed has unlimited power to buy bonds, but whether it always has the will to do so will depend on politics and other factors. Once it’s locked into a commitment, the stakes go up. For now, the markets – most importantly, foreign exchange markets – still trust the Fed. But, as the saying goes, trust is hard to earn, easy to lose.

ZIMBABWE ACCIDENTALLY LEAVES DOOR OPEN FOR CRYPTO. Here’s a recipe for creating a fertile environment for alternative payment systems: outlaw the system that everyone is currently using. When the Zimbabwean government made the nutty step of banning digital payments – used for 85% of transactions by individuals, due to severe shortage of cash – it clearly wasn’t trying to promote bitcoin. In forcing people to go to a local bank to redeem funds locked in popular payments apps such as Ecocash, its goal was to protect the embattled Zimbabwean dollar. In a statement, the Reserve Bank of Zimbabwe, said the move was “necessitated by the need to protect consumers on mobile money platforms which have been abused by unscrupulous and unpatriotic individuals and entities to create instability and inefficiencies in the economy.” The thinking is that Ecocash, which enables currency trading, is making it easier for people to dump the local currency. But here’s the thing: Ecocash, which said it suspended cash-in-cash-out functions (presumably because its banking lines will be cut) is still keeping in-app payment facilities open. And it said nothing about stopping its fairly popular service allowing people to buy cryptocurrency. Not surprisingly, since the ban “demand for bitcoin has skyrocketed,” according to African crypto news site, bitcoinke, with “sources claiming bitcoin is now selling at at 18% premium above the market rate.”

OF MONEY AND MYTHS. I’m reading Stephanie Kelton’s book, “The Deficit Myth.” In a future edition of Money Reimagined, I’ll have more to say on the most influential modern monetary theory proponent’s explanation of its ideas. But for now I’ll just say that, while I’m not likely to be a convert to all its prescriptions, it seems clear that MMT is widely misunderstood by folks on both the left and the right – also, very much by the crypto industry. The latter is perhaps because people in crypto tend to skew more to the metallist school of money, rather than to chartalism. Either way, a clearer grasp of what MMT is all about would, I believe, help improve the industry’s discussion around government, money, trust and how blockchain-based systems can integrate with the existing one.

How to Value Bitcoin: Bitcoin Days Destroyed

How to place a value on bitcoin? Its data are unfamiliar territory for many investors. Nearly half of investors in a recent survey said a lack of fundamentals keeps them from participating.

In a 30-minute webinar July 7, CryptoX Research will explore one of the first and oldest unique data points to be developed by crypto asset analysts: Bitcoin Days Destroyed.

We’ll be joined by Lucas Nuzzi, a veteran analyst and a network data expert at Coin Metrics. Lucas and CryptoX Research will walk you through the structure of this unique financial metric and demonstrate some of its many applications. Sign up for the July 7 webinar “How to Value Bitcoin: Bitcoin Days Destroyed.”

Relevant Reads

BIS Plans New Central Banking Fintech Research Hubs in Europe, North America. The Bank of International Settlements – the central bank to the world’s central banks – is getting serious about its money tech R&D centers, opening innovation hubs in Toronto, Stockholm, London, Paris and Frankfurt. A coordinated, standardized approach to developing central bank digital currencies? Danny Nelson reports.

Why the Stock-to-Flow Bitcoin Valuation Model Is Wrong. Maybe you shouldn’t be banking all your finances on a halving-driven appreciation in bitcoin this year. In this op-ed for CryptoX, contributor Nico Cordeiro picks apart one of the most commonly cited theories for why many people expect bitcoin’s baked-in quadrennial money supply decelerations to boost its price.

DeFi’s ‘Agricultural Revolution’ Has Ethereum Users Turning to Decentralized Exchanges. DEX’s, often touted as a fairer and safer way to trade cryptocurrencies, might finally have their use case: yield farming. In the past, as Brady Dale reports, most people haven’t wanted to self-custody, preferring institutions to manage the risks of holding their keys for them. But in DeFi, where people undertake dual borrowing-and-lending schemes to make big, quick returns on incentives and high interest rates, is better if you control the keys during the trade. And decentralized exchanges are seizing the opportunity.

‘Money Printer Go Brrr’ Is How the Dollar Retains Reserve Status. Our columnist Francis Coppola is here to tell you that you don’t understand how quantitative easing works. The Fed is not on some self-destructive missione here. Inflation? Not going to happen. The dollar’s demise? On the contrary; the Fed’s monetary rescue mission is what will keep the greenback atop its throne.

Senate Banking Committee Remains Open to Idea of Digital Dollar in Tuesday’s Hearing. If you want a measure of how far things have come in terms of the acceptability of the digital dollar idea in Washington from something that a year or so ago would have been a nutty, fringe idea, read the opening paragraph to Nikhilesh De’s writeup of this hearing: “Not every U.S. lawmaker is on board with the idea of a central bank digital currency (CBDC) or digital dollar, but no one explicitly rejected it during a hearing of the powerful Senate Banking Committee.”

The leader in blockchain news, CryptoX is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CryptoX is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.

Is Not")