It's become more expensive to use derivatives to insure against a decline in ether (ETH) than in bitcoin (BTC), indicating that market sentiment has shifted against the second-largest cryptocurrency by market cap, data from Deribit shows.

The sentiment shift comes after weeks of big money favoring ether over its larger peer.

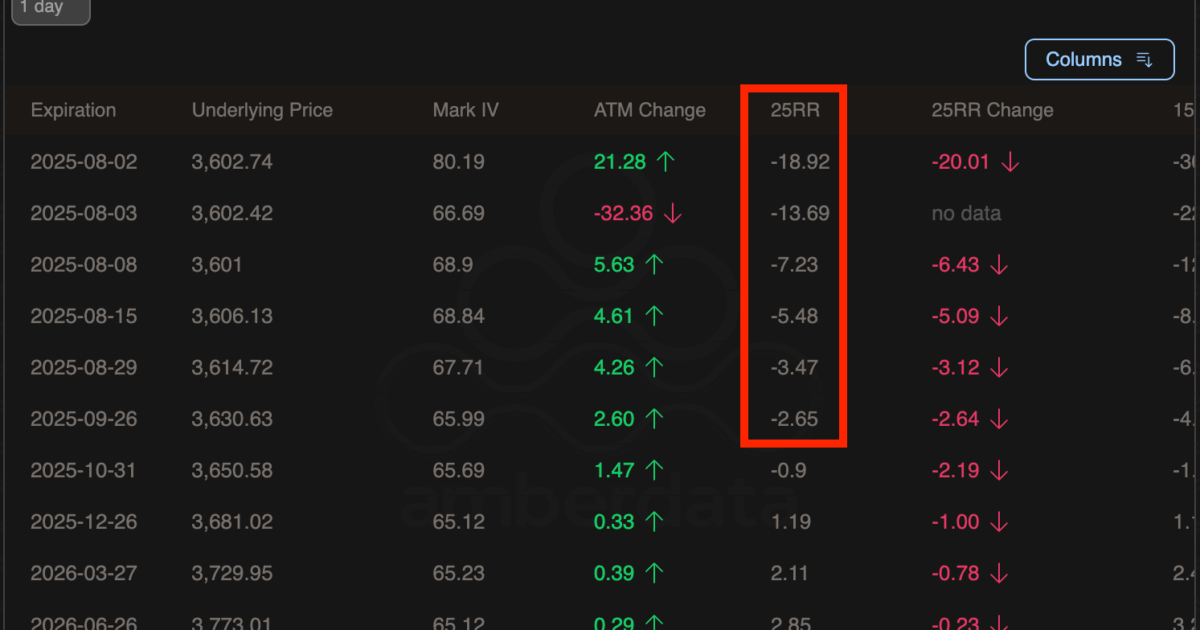

According to data from Amberdata, ether's 25-delta risk reversals for options expiring in August and September were trading at -2% to -7%. That means put options, which provide protection against drops in price, carry a 2% to 7% premium over call options, reflecting an apparent concern about a potential downside risk.

In comparison, bitcoin's short-term put options traded at 1%-2.5% premium to calls, suggesting relatively restrained downside fears.

A put option gives the purchaser the right to sell the underlying asset at a predetermined price on or before a specified future date. A put buyer is implicitly bearish on the market, seeking to hedge spot market holdings or profit from a price decline. A call buyer is implicitly bullish on the market.

")

The 25-delta risk reversal is an options strategy that comprises a long put position and a short call option (or vice versa) with a 25% delta, meaning the strike price for both options is relatively far from the underlying asset's market rate.

Risk reversals are widely tracked in the FX markets to gauge sentiment across time frames. Positive values represent bullish sentiment, while negative values suggest the reverse.

Ether, the native token of the Ethereum blockchain surged 48% in July, reaching a seven-month high of $3,941 and outperforming BTC's 8% gain by a wide margin. Most of the advance, however, occurred in the first half of the month, with the rally losing steam on concerns it stemmed purely from corporate adoption and lacked support from on-chain activity.

Ether was recently trading at $3,600, down more than 6% over 24 hours, while bitcoin had lost 3% to $114,380, according to CryptoX data.