TerraUSD (UST) flipping BinanceUSD (BUSD) for the third spot in the market capitalization list didn’t last long. The once-mighty stablecoin that powers the entire Terra ecosystem finds itself reduced to “Terra is more than UST” tweets. While no one knows for sure if LUNA can stage a comeback, UST will certainly go down as one of the algorithmic stablecoins that went kaput in the same fashion as Basis Cash — which Terra creator Do Kwon was allegedly a part of — and Mark Cuban-backed Iron Finance.

UST’s failure begs the question if algorithmic stablecoins are truly just doomed to fail? And, is fiat-backed or crypto-backed stablecoin the only way investors can find the most “stable” way to shield themselves from the crypto market’s volatility?

Pros and cons of different stablecoins

By now, most are aware of the types of stablecoins such as fiat-backed stablecoins, crypto-collateralized stablecoins and algorithmic stablecoins. There are also other types of stablecoins like commodity-backed and seigniorage, but the three mentioned above are the most popular.

Users have their reasons for preferring one kind of stablecoin over another. For instance, some prefer to use algo stablecoins because of their decentralized narrative. Others would go for fiat-backed cryptocurrencies like Tether (USDT) and USD Coin (USDC), even though they are centralized due to the private firms that maintain the equivalent fiat reserves of each issued token. Still, an advantage of fiat-backed coins is there is an actual asset backing the coin.

The stability of its peg will remain as long as there are verifiable holdings of such fiat reserves. Still, the most obvious risk here is a bank run scenario, which for Tether might be troublesome considering how it is largely exposed to commercial paper. Commercial papers are issued by large corporations and are a type of unsecured debt that can have a maturity of more than 270 days. A large number of redemption can render Tether insolvent, which is why it has slashed its commercial paper holdings over the last six months.

Crypto-collateralized stablecoins like Dai (DAI), on the other hand, are backed by an excess supply of another cryptocurrency, in this case, Ether (ETH). DAI requires a minimum 150% collateralization ratio, meaning that the dollar value of ETH deposited in a smart contract must at least be worth 1.5 more than the DAI being borrowed. For example, for a user to borrow $1,000 worth of DAI, they have to lock in $1,500 of Ether. If the market price of Ether drops to the point where the minimum collateralization ratio is no longer met, the collateral is automatically paid back into the smart contract to liquidate the position.

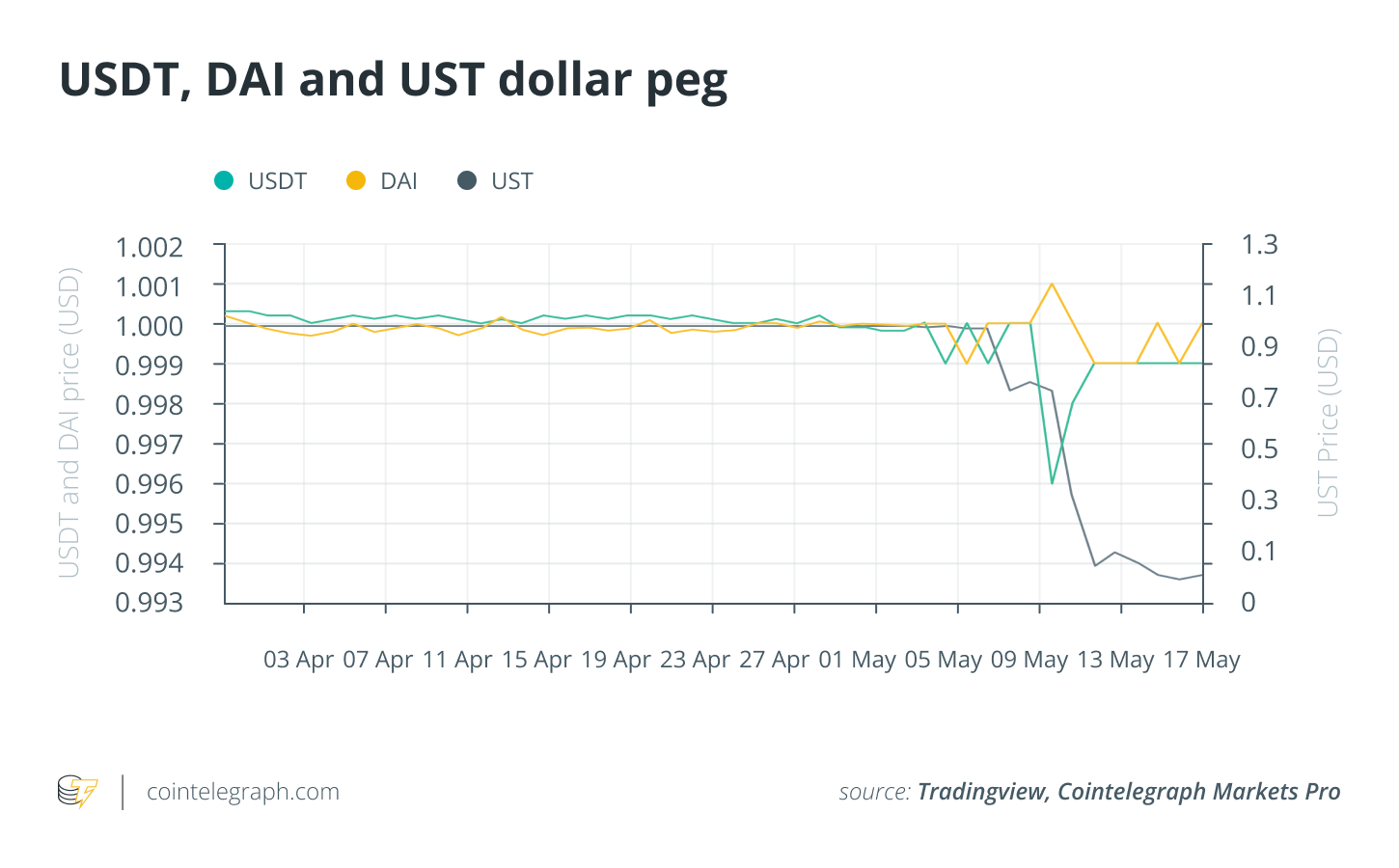

The case of UST

Stablecoins are, of course, meant to retain their value to their peg. However, what happened to UST was remarkably unprecedented and even threatened the collapse of the entire market. UST is a hybrid between an algo stablecoin and a crypto-collateralized stablecoin. When the price of UST moves above its dollar peg, users are incentivized to burn $1 worth of LUNA for UST to sell at a profit. When UST falls below the peg, users can burn UST in exchange for a discounted LUNA. It became crypto-backed since the Luna Foundation Guard acquired great amounts of Bitcoin (BTC) collateral as a contingency plan. This, as it turned out, was ineffective, and the last few holdings of BTC and other assets were allocated to smallholders as compensation.

Terra’s collapse started with the large withdrawals on Anchor Protocol on May 8. Millions of UST were pulled out from the protocol and quickly sold, causing a downward spiral. What ensued was more panic. The algorithm eventually couldn’t respond quickly enough — by burning LUNA — to the rapid decline of UST’s value.

In hindsight, the evidence was apparent since the primary demand for UST was only derived from the demand in Terra’s Anchor Protocol. The low trading volume of UST suggests that users are more interested in keeping it in the protocol than actually utilizing it for trading.

DAI holding steady

Amid the panic, with Tether even briefly losing its peg to the United States dollar, DAI had actually remained relatively stable. At one point, USDT dropped to about $0.994 on May 9, while DAI rose to $1.001. DAI has even been hailed recently as “the” true decentralized stablecoin.

Having existed since 2017, DAI has survived many extreme conditions in the market, which no algo stablecoin has ever managed to do. Yet, there can never be a shortage of risk, especially in the crypto market.

Cryptox’s Market Insights Newsletter shares our knowledge on the fundamentals that move the digital asset market. The newsletter dives into the latest data on social media sentiment, on-chain metrics and derivatives.

We also review the industry’s most important news, including mergers and acquisitions, changes in the regulatory landscape, and enterprise blockchain integrations. Sign up now to be the first to receive these insights. All past editions of Market Insights are also available on Cryptox.com.